Much of the recent market reaction to AI has been framed around the idea that incumbent software and data companies are about to be disrupted. In my humble opinion, that framing overlooks how these businesses actually operate and there is something slightly odd about the way the market is framing the situation.

The sell-off assumes that AI disrupts these businesses, but it also assumes that the businesses themselves just sit there and do nothing about it. These are not small companies run by people who have never heard of ChatGPT. They have enormous research and development budgets, deep technical talent and, crucially, the data that AI needs to be trained on and function. Many of them are already well-advanced in building AI into their products. The idea that a startup with a clever model but no proprietary data will simply waltz in and take their customers ignores the reality of how enterprise software works: long contracts, deep integration, high switching costs and regulatory requirements that do not disappear just because a new tool exists.

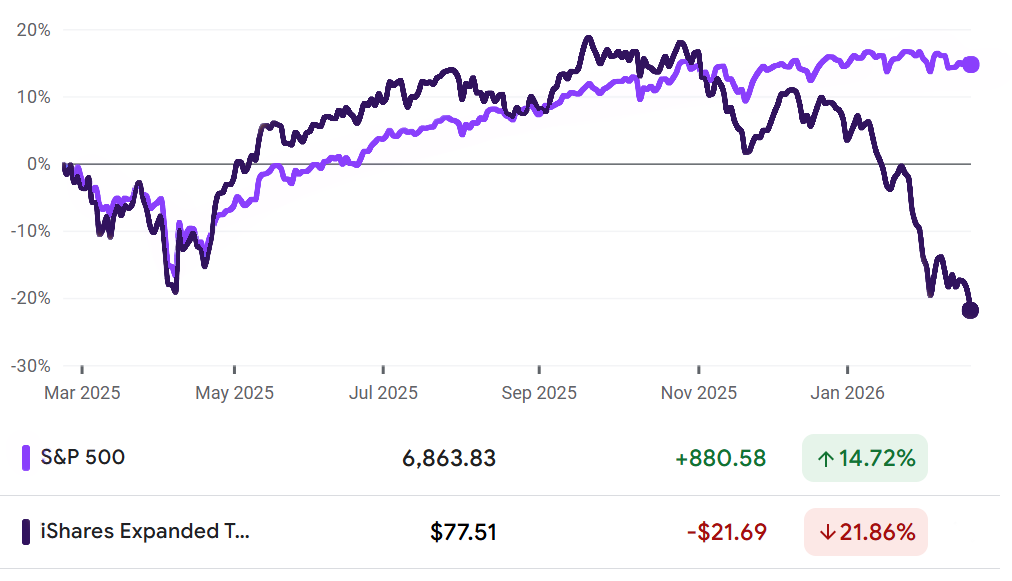

There is no doubting that the software and data sector has had a difficult few months. AI disruption fears have weighed heavily on the market and what have historically been some of the highest quality, most cash-generative businesses in the world are trading at multi-year lows. The S&P North American Software Index had its worst monthly decline since January 2008. Cloud computing stocks are down around 20% year-to-date. JPMorgan estimates that software companies have lost around $2 trillion in value over the past year, which they describe as the largest non-recessionary 12-month drawdown in over 30 years.

One of the most recent catalysts was AI company Anthropic's launch of new legal and enterprise AI tools, which hit anything connected to legal software, data analytics or business services. But this was just the latest in a series of AI-induced sell-offs that have been building since mid-2025. Each new product announcement from the likes of Anthropic, OpenAI or Google has been met with the same reaction, which has been to sell everything that looks like it could be disrupted.

The bear case is straightforward. AI commoditises software, erodes pricing power and makes legacy data businesses less relevant. For some companies, that concern will probably prove justified. Businesses that essentially sell workflow tools, task automation or basic SaaS products face a genuine challenge. If an AI agent can deliver similar functionality at a fraction of the cost, the value proposition of a hefty annual subscription starts to look questionable.

My view is that the market is painting everything with the same brush, and that is where it gets interesting. There is an important distinction between companies that sell software tools and companies that own proprietary, structured data built up over decades. Software can be replicated. AI does not replace it, it needs it. The businesses that own the best datasets are not the victims of the AI shift, they are the enablers. That distinction has been largely overlooked in the sell-off.

Take the information services space as an example. Companies like RELX, an information and analytics company that owns LexisNexis (legal research) and Elsevier (science, technical and medical research), are being valued by the market as though they are generic software businesses facing obsolescence. In reality, their competitive advantage is rooted in proprietary, curated datasets built up over decades. An AI model cannot simply replicate that. It needs exactly that kind of structured, high-quality data to function effectively. These businesses are not being disrupted by AI, they are deploying it into their own products and monetising it.

This gap between sentiment and fundamentals has been increasingly notable in recent results, with businesses delivering strong organic growth, expanding margins and increasing cash returns to shareholders, yet trading well below where they were six months ago. Retention rates across the sector remain high. Clients have not stopped buying, they have in some cases slowed purchasing while they assess how AI fits into their own organisations. That is a different thing from structural disruption. The fear is in the price.

For investors, this is worth paying attention to, and without trying to state the obvious, share prices do not just move based on what a company is doing today, they move according to what the market thinks might happen next. When uncertainty rises, the tendency is to price in the worst case well before it actually plays out. That can create situations where valuations completely disconnect from what is happening on the ground. In the long run, fundamentals tend to win, but in the short term sentiment can take over and the two can stay out of sync for longer than one might ideally like or expect.

Now, I am not saying that every software business will come through this period unscathed – far from it. As with every revolution (and AI is a revolution, and happening much quicker than I think many realise), there will be casualties, and my view is that those reselling commoditised functionality with no real data moat are vulnerable. But the broad nature of the sell-off has created a situation where high-quality businesses with sticky recurring revenues, deep proprietary data assets and the ability to deploy AI into their own products are trading at valuations we have not seen in years. In my experience, these periods of broad-based selling are where the best long-term opportunities tend to be found.

RELX is a constituent of the Advisory Stockbroking Approved List, and the author also has a personal holding in the company.