As we look back over 2025, we see a year of change reflected in how the Titan Global Blue Chip’ Fund’s performance has responded to markets. The defensive characteristics that previously dampened volatility have given way to a more correlated profile which, at times, delivered good upside during risk-on phases. This quarter’s Insights deviate somewhat from the normal format as we explain the process changes we’ve made, why we felt these were necessary, how the strategy is positioned today and why investors should stay the course.

We have written extensively about the challenges the strategy faced, particularly through 2024 when performance fell short of our expectations, and in 2025 when we implemented changes. The core issue wasn’t our philosophy (large-cap quality, investing alongside dominant trends shaping the world around us), but rather that we initially underestimated the extent of the changes we were witnessing in market structure and investor time horizons as we considered them to be temporary distortions rather than what we now recognise to be features. Rather than expect the market to revert to our preferred regime, we accepted the operating environment had changed (potentially for the long term) and made the necessary adaptions to improve performance.

Controlling The Controllable

Single-stock volatility around new information flow has become almost comical. Moves of 5–10% are treated as “normal” and, while 20–30% drawdowns are still outliers, they are occurring more frequently.

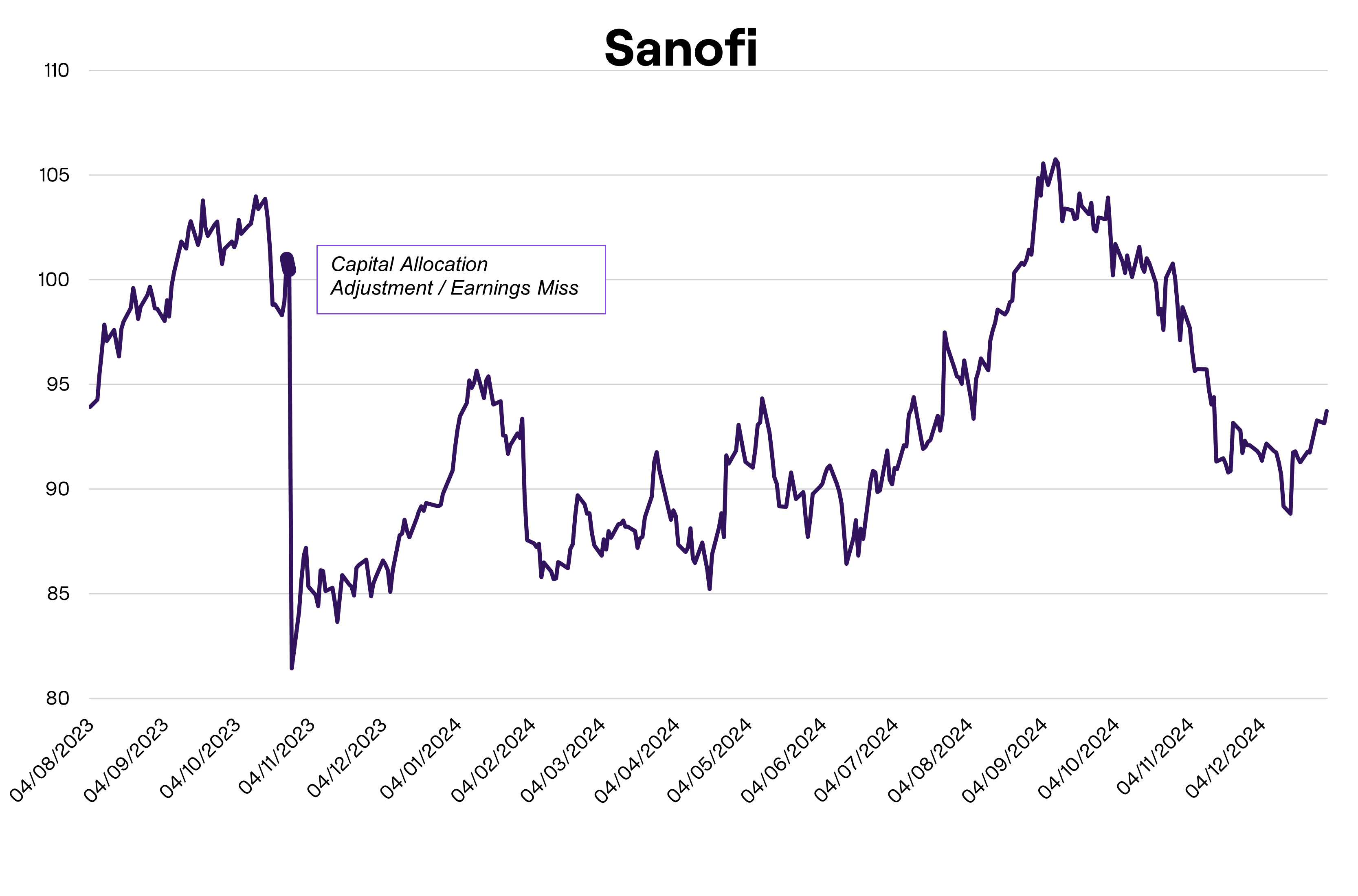

We experienced this first-hand in Sanofi’s Q3 2023 update. Heading into the announcement investors expected a continuation of mid-single-digit earnings growth, underpinned by strong uptake of the blockbuster drug, Dupixent, and a similar growth profile to be signposted for the year ahead. Instead, management marked earnings progress down to essentially flat as they accelerated investment into the pipeline to secure growth through the rest of the decade. We saw that as a sensible long-term reallocation of capital. The market’s response - down ~20% - suggested otherwise. A 5% position in what we considered a cheap, defensive pharmaceutical business translated into roughly a ~1% haircut to performance in a single day.

Compiled by: Titan Wealth CI

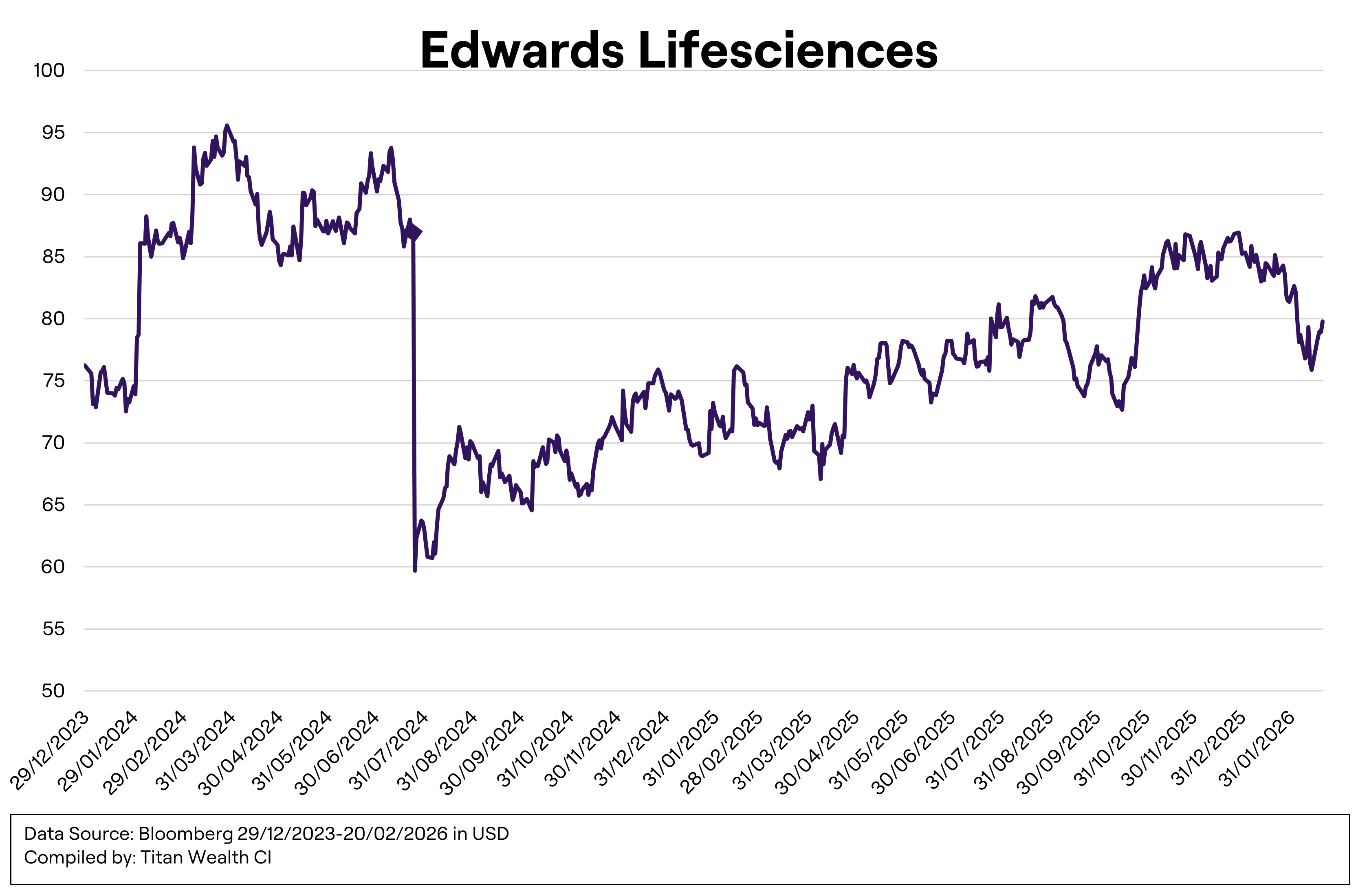

Edwards Lifesciences got the same treatment in Q2 2024 when management flagged a slower-than-expected cadence in structural heart procedures. The issue wasn’t competition unexpectedly taking share or a product recall. It was hospital staff shortages causing operations to be postponed - not cancelled. You can’t live with a faulty heart valve for long; you eventually have to get it sorted. Edwards’ best-selling products are minimally invasive transcatheter technologies that can replace valves across the heart. They are a big win for patients - faster recoveries, fewer complications, shorter stays, and immediate improvements in quality of life. They’re also a big win for payers, increasingly viewed as economically dominant because they reduce costs across the care pathway: lower admissions, reduced post-acute care and fewer rehospitalisations and follow-up needs. All of which, apparently, pales into oblivion when year-end earnings targets are revised lower.

Compiled by: Titan Wealth CI

As we held a 3% position, we faced a ~1% headwind from a ~30% downdraft in a single morning. Sanofi and Edwards are not unique events; they are clear-cut case studies of a market that increasingly reprices on guidance risk and positioning, not long-term value creation. These outlier reactions are becoming less outlier and more mainstream.

We now believe a key driver is how modern institutional trading has evolved around earnings. Many hedge funds expend enormous energy forecasting the print and positioning for the move - long or short - because capturing the reaction matters as much as (and often more than) being right about the business. This is amplified by the dominance of “pod shops” and multi-manager platforms, which can account for the majority of institutional activity on earnings days. Their short time-horizon views, concentrated bets and algorithmic momentum strategies are frequently detached from deep fundamental analysis and can intensify price movements.

The result is an environment of elevated dispersion – between and within sectors – rather than broad, index-wide drawdowns. Capital increasingly concentrates in dispersion trades, rotations accelerate, winners are rewarded more quickly, losers are punished harder and incentives

drive even greater concentration as “what worked” attracts more size. In this environment, focused portfolios can be hit simply by being on the wrong side of a single earnings announcement, even when the long-term thesis remains intact.

While this can create opportunities to add to positions, the problem is that the damage has already been done. More importantly, it’s not a given the market has overreacted. There are plenty of examples where a >20% reaction is the start of continued weakness, not the end of it. We have experienced this ourselves, thinking fundamentals were improving and valuation was on our side, only to watch further losses mount as sector-wide negative momentum took hold and prices continued to fall.

Broad-based selling is becoming more common as views are expressed through ‘baskets’ of grouped exposures rather than individual securities. Recent examples include the pressure on healthcare stocks created by anxiety over the incoming Trump administration, and the more recent selloff in software stocks as AI model development and application threatens previously assumed competitive moats. Again, the indiscriminate nature of these initial moves can create opportunities for active investors able to distinguish between franchises where competitive advantages are genuinely at risk and those where resilience is likely to prove greater than market pricing implies.

This combination – bigger earnings reactions and more frequent value traps – forced a pragmatic response at the portfolio construction level. We have reduced overall stock position sizes to limit the portfolio impact of outsized single-day moves and increased the number of holdings in order to remain fully invested. As a result, the strategy now consists of approximately 40–45 holdings.

We’re also increasingly focusing on price action and relative performance as indicators of risk. We are not traders acting on technicals, but there are clear instances when stocks enter definitive downtrends (or uptrends) and fighting this price action can become costly. Valuation remains important, but it has become a weaker timing tool in a market that increasingly prioritises near-term outcomes.

Feedback from investors is that underperformance, whether understood or not, is less tolerated, and time preferences have shortened materially. We have written about this previously, citing how holding periods have fallen to less than a year (although we suspect they may now be even shorter).

We view this as a feature of today’s equity market and, challenging as it may be, it is something all investors will have to navigate.

Compounding this is the continued rise of passive investing, which has shifted from a low-cost alternative to the dominant force shaping market structure, creating the set of dominating mega-caps. What was designed to track the market has, in many respects, become the market. As capital flows mechanically into index-like products (particularly ETFs) - driven by retirement structures, regulatory defaults, and fee compression - the marginal buyer increasingly operates according to rules, rather than fundamental assessments of valuation. This dismantles the price discovery process that valuation-based investing relies on as flows are applied pro-rata, with the largest positions capturing more of the economics. Consequently, the big get bigger, ownership and influence concentrate further and momentum effects are amplified in bull markets as flows become the primary driver at index and sector level.

The trade-off is heightened fragility beneath the surface. Liquidity looks abundant at first glance as spreads are tight and indices feel stable, but in stress the “real” liquidity in the underlying stocks can evaporate quickly as the same mechanical flows reverse, market makers step back (especially in the growing volume of options) and correlations jump (dispersion collapses). In short: passive dominance has altered the market’s DNA, creating a surface-level efficiency while introducing systemic distortions and vulnerabilities that investors wilfully ignore.

Financial Innovation, Leverage And The Rise Of “Desperation Capital”

Financial innovation, the growth of leveraged products and the rising popularity of what we’d call “desperation capital” probably deserve their own standalone commentaries. However, for the purposes of this note, the point is simple: all three reinforce the same market outcome - higher volatility and shorter time horizons.

The modern market offers an ever-expanding toolkit for expressing views with asymmetric payoffs: zero-days-to-expiry options, leveraged and inverse ETFs, single-stock derivatives, structured products and systematic strategies that turbocharge momentum. The barrier to placing a large bet has fallen, the speed at which those bets can be put on (and taken off) has increased, and leverage is no longer a specialist instrument - it’s increasingly embedded in the product wrapper.

This impacts market structure and participation behaviour because leverage doesn’t just magnify returns, it creates anxiety over losses and compresses time. It forces participants to care less about whether they’re right over three years, and more about whether they’re right by expiration. When positioning is crowded and leverage is high, small surprises become big moves, stop-losses become forced selling, and what should be a contained drawdown can turn into a cascade.

“Desperation capital” represents the behavioural layer on top of these structural forces. It reflects the need for the market to deliver returns quickly in order for investors to catch up, keep pace, or recover prior losses, and it pulls behaviour toward shorter-term, higher risk-reward outcomes rather than the long-term compounding of capital. In this environment, investors start to behave more like punters, where short-term outcomes are dominated by narratives and market positioning, whilst volatility becomes the price you pay to participate.

These dynamics are not challenges that we can ignore. We can’t control the earnings surprise, the positioning adjustments or the mechanics of passive flows. What we can control is how much any one event can impact our strategy and how quickly we recognise when the outcomes differ from our expectations. That is why, in addition to reducing individual position sizes, we have broadened the portfolio out and added additional performance monitoring of stock prices relative to sector peers and the broader market – to flag underperforming stocks as an explicit risk control signal.

To combat the impact passive dominance can have on relative returns, we’re not precious about which stocks dominate an index - but we are more aware of our positioning relative to the market and how our holdings are behaving versus their sector peers. If a stock is persistently underperforming its peer group, as identified in the cross-sectional momentum analysis described above, we ask why, return to the research and test whether we’ve missed something. In 2024, a number of our holdings performed well, but our willingness to maintain positions in stocks that were persistently fighting the trend meant their overall contribution was reduced.

The way performance is evaluated, combined with the ease with which clients can reallocate capital, means there is limited tolerance for extended periods of underperformance. Expecting investors to exercise patience in such circumstances is neither realistic nor appropriate. The feedback we have had is clear: investors expect active managers to respond to changing market dynamics and deliver outcomes within the prevailing environment, rather than hear the complaint it isn’t “their market”.

Whilst we don’t want to get shaken out of good companies exposed to compelling trends, we do need to listen when markets speak. We can control this through closer monitoring and faster action when we believe a mistake has been made. Often those mistakes are about timing rather than investment thesis or business quality, and monitoring stock performance relative to peers and the broader market can help identify when something is genuinely broken versus merely unloved.

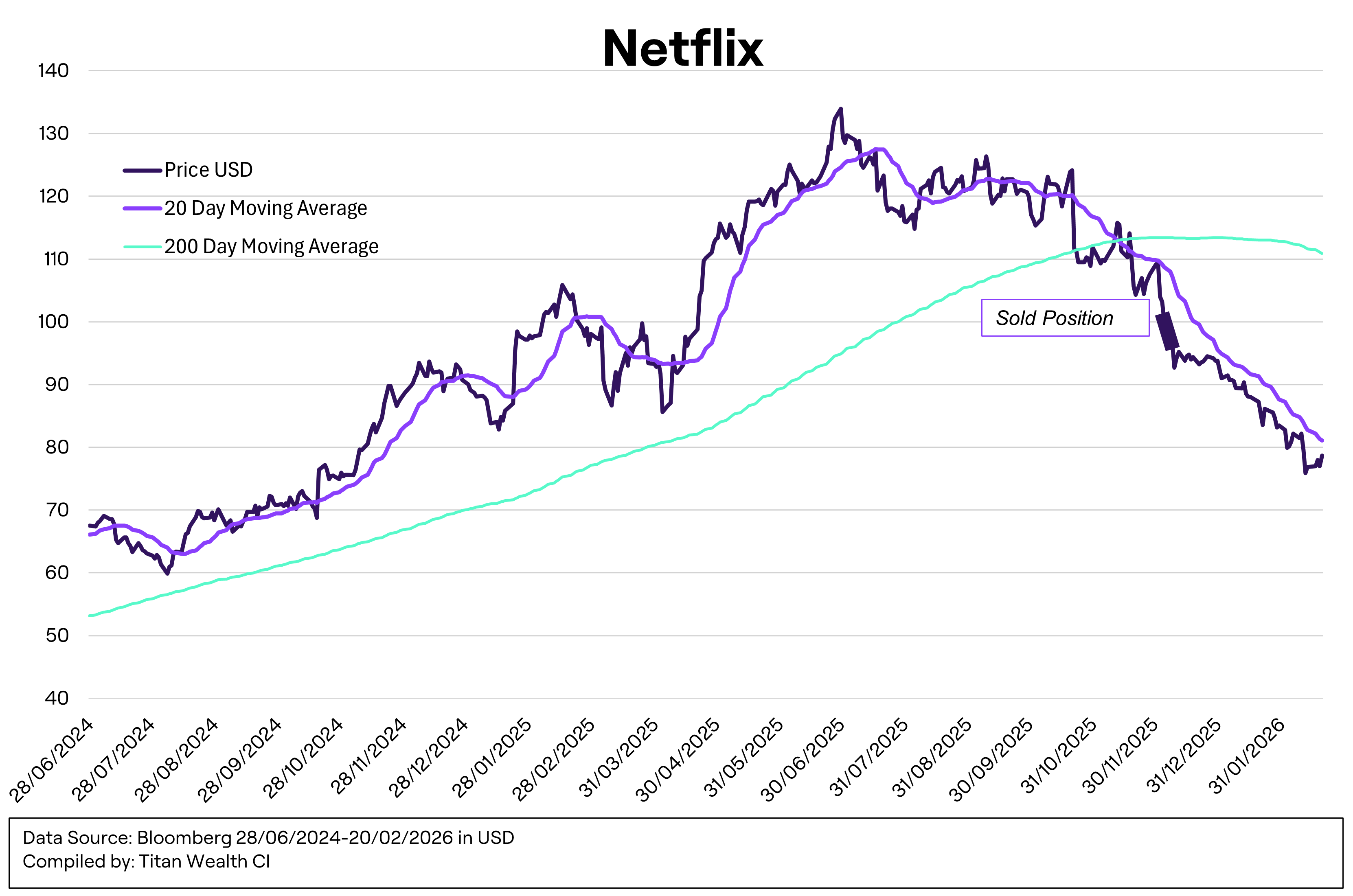

We use Netflix as a good example of how unfolding developments impact price. For years we backed management’s view that Netflix had a large organic runway, driven by multiple revenue levers on top of its formidable ‘glocal’ content production engine: the ad-supported tier, gaming, fandom and engagement initiatives and a broader push to widen monetisation without breaking the product. The market agreed. Even when quarters were messy, the stock was consistently bought on weakness, and new highs kept forming - a classic “reward the long-term plan” narrative.

That tone shifted around the July and October earnings windows as rumours grew on Netflix’s interest in Warner Bros. The potential deal materially altered the investment proposition. First, it challenged management’s credibility – Netflix had long positioned itself as a builder, not a buyer. Second, an acquisition of that scale would not be incremental; it would change the balance sheet, the risk profile and the operating focus (and we’ve lived through enough Disney-style integration headaches to know these are rarely clean).

Once it became clear Netflix was the front runner for the Warner streaming and studio assets, we exited. The above chart validates this decision; the stock had by then definitively broken its uptrend, having rolled over and slipped below its longer-term trend measure - the kind of price action that usually signals a change in how the market is underwriting the story, not just a temporary wobble.

Compiled by: Titan Wealth CI

With the stock now in a clear downtrend (note how it’s trading consistently below the short-term moving average), we’re happy watching from the sidelines. What would bring us back? First, price stabilisation - the stock needs to stop falling. Second, fundamental confirmation that management’s actions are aligned with shareholder value rather than empire-building. Third, valuation and expectations - understanding what the market is now pricing in, and whether this is achievable.

Credibility matters - if management has dented trust, we need stronger evidence before re-underwriting the story. The counterpoint is that Netflix has earned real benefit of the doubt over time - they’ve executed pivots exceptionally well. So, we’re not done with Netflix. We’re just not desperate to be involved at the moment, particularly in a market where opportunity is abundant.

A related adaptation has been a more explicit pivot towards our themes. Historically, themes were a secondary lens behind business quality and valuation - useful for context, but not the primary driver of capital allocation. That hierarchy made sense in a market that consistently rewarded steady compounding. Today’s market behaves differently. It increasingly rewards opportunity - large and growing addressable markets, accelerating profit pools, and businesses positioned on the right side of powerful adoption curves - often ahead of the neatest “value proposition” on traditional multiples. We prefer the old rulebook, but this is the one the market would appear to be preferring at present.

As a result, we now aim to keep the Titan Global Blue Chip Fund positioned at the forefront of cutting-edge themes and more growth-oriented profit pools, while still insisting on business quality. Our valuation framework has evolved alongside that shift: less margin of safety in the classic sense, and more forensic work on what expectations are embedded in the price, understanding the market’s perception, and how realistically achievable we think they are. That expectation-led valuation then feeds directly into position sizing and a more qualitative assessment of relative value - not just whether something is cheap, but whether the risk/reward is attractive versus other opportunities competing for capital.

Fund Changes

To summarise what has and hasn’t changed:

- Markets have shifted. Single-stock moves are bigger, time horizons are shorter and flows/positioning can swamp fundamentals.

- We can’t control these market dynamics. Instead, we have adapted by reducing idiosyncratic risk (smaller positions, more holdings), using price action and relative performance as risk signals and being faster to act when a thesis is invalidated by the market.

- We’re also more deliberate about leaning into the themes where profit pools are growing, with valuation judged less by cheapness and more by what expectations are priced in - and whether they’re realistic.

- Finally, it’s important to note that we aren’t having to compromise on the quality of what we own in order to access the growth opportunities. We’re still looking for best-of-breed core holdings, and where there is cyclicality or premium valuations, we’re deliberate in the risk we assume. The world is changing and the investment set-ups are coming thick and fast for those with the flexibility and willingness to recognise them.

Building On Foundations Laid In 2025

One of the most tangible changes has been portfolio construction. We expanded the opportunity set to better capture areas we previously underweighted. In a more fractured world - where supply chains are exposed as fragile and governments are prioritising security, resilience and domestic capability - a large rebuild cycle is now underway. Industries that have been hollowed out and underinvested in for decades are suddenly back at the centre of capital allocation. That creates a powerful opportunity set we want to capture alongside the better-known growth engines.

To express this more clearly in the portfolio, we formalised a new investment theme: changing world. It gives us a framework to map the reindustrialisation and security cycle, identify where profit pools are expanding, allowing us to build exposure with intent.

Populating the theme was the easy part. Funding it was harder - both in terms of letting go of legacy holdings and getting entry timing right in a market that reprices quickly. We used 2025 to build the foundations and establish positions.

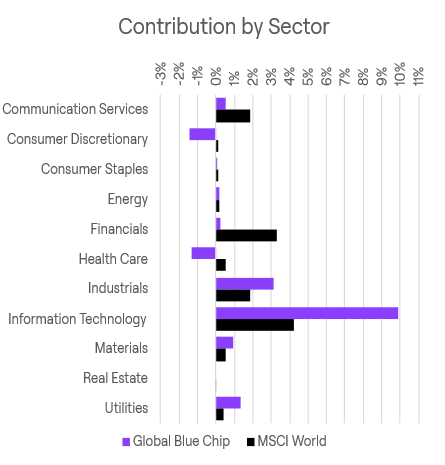

While performance contribution last year was dominated by our technology investments in AI hardware, we expect 2026 to look more balanced, with returns deriving across a broader set of themes and sectors as the opportunities within our changing world theme mature.

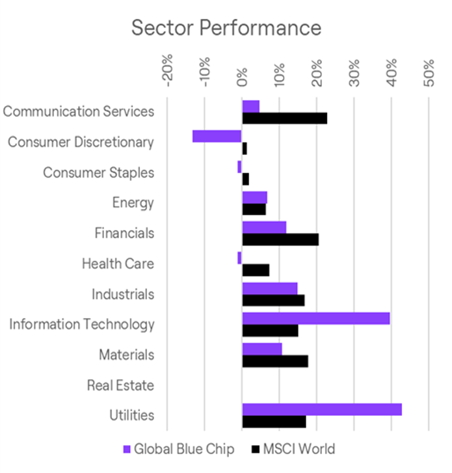

2025 Aggregate Positioning, Performance and Contribution

Data Source: Bloomberg 31/12/2024 – 31/12/2025

Expectations For 2026

We expect the sub-themes within our changing world theme to play a larger role in driving returns as US statecraft and fiscal agendas translate into real-world spending, subsidies, reshoring incentives and defence modernisation. At the same time, the AI infrastructure build-out will most likely surprise again to the upside as a reinforcement loop materialises with accelerating adoption - but the market is becoming increasingly sensitive to AI’s disruptive potential, and that sensitivity is already reshaping sector leadership. Investors should expect more volatility and, by extension, potential opportunities to be created.

We’ve already seen that most clearly in software. After decades as the market’s darling – high margins, recurring revenue and valuations built on the assumption of “limitless” growth – the regime has shifted. AI is now challenging the assumptions embedded in those multiples, and the de-rating has been brutal. We do not believe AI will replace every software product, but it will displace some, compress pricing power in others and force new commercial models that reallocate economics across the value chain.

That disintermediation risk won’t stop at software. Any business whose profit is anchored in solving friction - between a human and a service, or an employee and a workflow - is exposed to some degree of repricing as AI lowers switching costs and increases substitutability. In 2026, staying alert to these threats, consideration of second-order impacts and the avoidance of the most vulnerable franchises will be as important as owning the companies and themes that continue to benefit. At the same time, identifying the real value amongst the areas most impacted may also be an attractive source of return. Below, we set out how the portfolio is currently positioned and what we’re looking at and actively avoiding.

Changing World

Power and grid infrastructure

AI-driven demand for reliable baseload power is showing up in tighter electricity markets, rising forward power prices in constrained regions and an accelerating cycle of grid upgrades. This has created a huge opportunity across the value chain, from power production through to its distribution. The strategy has exposure to companies involved in the direct production of power, electricity distribution, grid infrastructure equipment providers, service providers and energy commodity producers.

Commodities and strategic materials

The commodity complex continues to reflect the consequences of decades of underinvestment, amplified by tighter regulation, an uneven transition agenda and the outsourcing of midstream processing. Demand is surging as the AI buildout and government infrastructure projects drive commodity consumption across the periodic table. At the same time, supply is constrained, lead times are longer and domestically viable, readily accessible projects are scarce. China’s dominance in the midstream processing of critical rare earth materials — including refining, smelting, and conversion — and its increasing ability to exert gatekeeper influence over key supply chains represent an additional source of vulnerability. The US is now responding with purpose; stockpiling reserves, making strategic investments, deregulating permitting legislation and increasing its willingness to support domestic supply chains. Improving the investment environment is now a clear priority to entice capital back into an industry that has been starved of it and as a consequence has left vulnerability in its wake. As demand ramps and cash flows grow, we expect a reinvestment cycle within the commodity complex and an increasing demand for the modern day “picks and shovels” that feed into miner’s operations.

Gunboat diplomacy and defence modernisation

Geopolitics is no longer a background risk. It is actively reshaping global affairs and capital allocation. In a world where globalisation and cooperation has rapidly given way to security of supply, geopolitically driven flashpoints are likely to increase from Greenland to Iran. Venezuela, Ukraine, Taiwan and Israel are all reminders that threats (real or perceived) will create uncertainty and a need for security. NATO members signalling higher defence and infrastructure commitments reinforces the direction of travel. The more significant shift, however, relates to the priorities of modern warfare. The conflict in Ukraine has demonstrated the effectiveness of autonomous drones and missile systems, as well as the importance of countering them through integrated architectures encompassing sensors, data, communications, decision advantage, and electronic warfare – all designed to compress the decision-making cycle. Our focus is on the enabling stack: C6ISR architectures and the systems that enhance detection-to-decision-to-action speed and operational resilience. Competing monetary systems and currency debasement.

We also expect the year to keep delivering evidence of parallel monetary rails being built alongside, and potentially threatening, traditional banking. Stablecoins, tokenised deposits and on-chain settlement are moving from concept to deployment - reducing friction, enabling 24/7 money movement, and changing who captures economics in payments and financial infrastructure. Further information on the CLARITY Act will offer a clear signal on the direction of travel for stablecoins, a tool that could radically reshape global liquidity and demand for US dollars. At the same time, governments face rising funding needs, and “debasement by necessity” remains a plausible path of least resistance. That supports a world where hard assets retain a structural bid.

Global Consumer

Consumer markets are undergoing disruption on multiple fronts, alongside a challenging macroeconomic backdrop as lower- and middle-income families struggle with the rising cost of inflation. In a more fractured world, China, and by extension parts of ASEAN, is becoming a more competitive and less accessible arena for Western brands, while supply chain sustainability, inventory mistakes and uneven demand keep margins under pressure. Agentic AI and the birth of the agentic shopper is also creating anxiety amongst investors. Who needs aggregators and payment processors in a world where machines tackle tedious jobs with ease and whose focus is simply the most efficient and cheapest way to meet the preferences of their programmer? This is an incredibly difficult environment to master and, in this context, categories characterised by essential demand, such as personal and household care, together with logistics and distribution networks that enable the physical movement of goods, appear comparatively more resilient.

Ageing Population

Healthcare is beginning to emerge from a multi-year sentiment slump. Ageing populations continue to drive demand structurally, although the sector’s attractiveness remains influenced by the current political environment. The improving tone across pharmaceuticals, helped by a string of tariff deals negotiated between the Administration and industry participants, has helped improve sentiment. For the rest of 2026, along with looking for signs that the sentiment shift may be lifting medical devices and life science businesses as well, our focus is on businesses where (i) innovation drives growth, (ii) margins can expand through scale and mix, and (iii) products materially improve outcomes and reduce costs - the type of value creation that payers will ultimately gravitate to, even if the market’s short-term attention span is diverted by quarter-end numbers and year-end guidance.

Technology & Innovation

Our focus remains predominantly on the rails which AI will be built and scales. That includes GPU and ASIC designers and the companies that provide the tools and equipment enabling fabrication. There are clearly identifiable bottlenecks within this value chain; however, access to these areas increasingly requires accepting elevated valuations, as markets tend to reprice structural constraints rapidly in periods of heightened demand. However, we’re constantly scanning for opportunities and reviewing opportunities emerging within the software sector. AI’s disruptive narrative has resulted in dramatic software valuation shifts as investors question the limitless growth narrative. As this adjustment progresses, we expect attractive opportunities to emerge in businesses with the most compelling long-term propositions.

The Global Blue Chip Investment Case

We’re investing through a period of structural change – geopolitically, economically and socially – and that is exactly when a thematic, quality-biased approach can offer the most edge in our opinion. Our key focus is to identify the opportunities being created by the direction of capital for strategic or commercial purpose. The strategy is anchored in businesses with resilience, liquidity and durability as we seek to monetise those opportunities. Just as importantly, our process is now more open-minded and adaptable, which matters in a world where change is the only constant.

We also believe the current regime continues to favour growth and real assets. Monetary conditions are unlikely to become meaningfully restrictive for long without creating financial stress; the system is fragile and markets remain central to the wealth effect. Fiscal policy is structurally biased toward spending over austerity, and in a credit-based economy growth relies on credit expansion. Economies are increasingly on a form of war footing, and state capitalism is becoming explicit: grants, subsidies, strategic stakes and regulatory change are now part of the playbook.

Against this backdrop, asset prices may continue to inflate, widening the divide between asset owners and non-owners and pushing more participants toward what is performing rather than what offers protection. That doesn’t mean fundamentals no longer matter, but the market is rewarding investors differently and we intend to be on the right side of that change by positioning the strategy accordingly.