“Don’t let it bring you down,

It’s only castles burning…”

Neil Young, “Don’t let it bring you down” (1971)

The year began much as 2025 ended.

Markets were constructive. The US dollar was weakening, and capital was beginning to flow more meaningfully into Europe, including the UK, as well as emerging markets and hard assets. Gold had been on a remarkable run, reaching record highs in late January and even crypto found renewed support.

This was all underpinned by a relatively benign macroeconomic backdrop: inflation appeared to be moderating and, with it, the prospect of lower interest rates later in the year was becoming increasingly realistic. Both equities and bonds responded well through January and into February, reflecting a growing confidence that the path ahead, whilst never entirely smooth, might at least be manageable.

That narrative has, for now, been interrupted.

The decision by President Trump to launch military action against Iran shifted the focus of markets abruptly. Oil prices moved sharply higher, with Brent crude surpassing $100 a barrel for the first time in four years, and with that, inflationary concerns re-emerged. Expectations for lower interest rates were pushed out, bond markets weakened and equity volatility returned. The US dollar, having softened earlier in the year, found support as investors sought relative safety.

Interestingly, not all traditional relationships have behaved as one might expect. Gold, which had been particularly strong earlier in the year, sold off sharply through March. This is partly a story of profit-taking after an extraordinary run, and partly a reminder that when multiple forces are at play simultaneously, markets do not always respond in a linear or predictable fashion.

At the centre of all of this sits energy.

The Strait of Hormuz, through which approximately a quarter of the world’s seaborne oil passes each day, has been severely disrupted. The withdrawal of insurance, and the resulting increase in transport costs, has effectively brought shipping to a near standstill.

Higher energy costs rarely remain contained. They work their way through supply chains, feeding into food prices, manufacturing costs and ultimately inflation. That, in turn, influences interest rate expectations, economic growth and confidence. It is a well-worn chain of cause and effect, but one that markets are having to reprice once again.

It is also worth remembering that this is not the first time we have faced such a scenario. Energy disruptions have occurred repeatedly over the past fifty years, from the Yom Kippur War in 1973 and the Iranian Revolution in 1979 to the Gulf War in 1990. Each brought volatility and, at times, real discomfort. Each was also ultimately absorbed as economies adjusted, supply responded and behaviour changed.

None of this was in the script for 2026. The attack on Iran represents, in the truest sense, a Black Swan — an event so unlikely that few had genuinely planned for it and one that, almost by definition, could not have been priced into markets in advance. As the strategists say, it is the risks you don’t see coming that tend to matter most.

Which brings to mind Mike Tyson’s rather more direct take on the subject, “Everyone has a plan until they get punched in the mouth”. Markets, like boxers, are having to adjust.

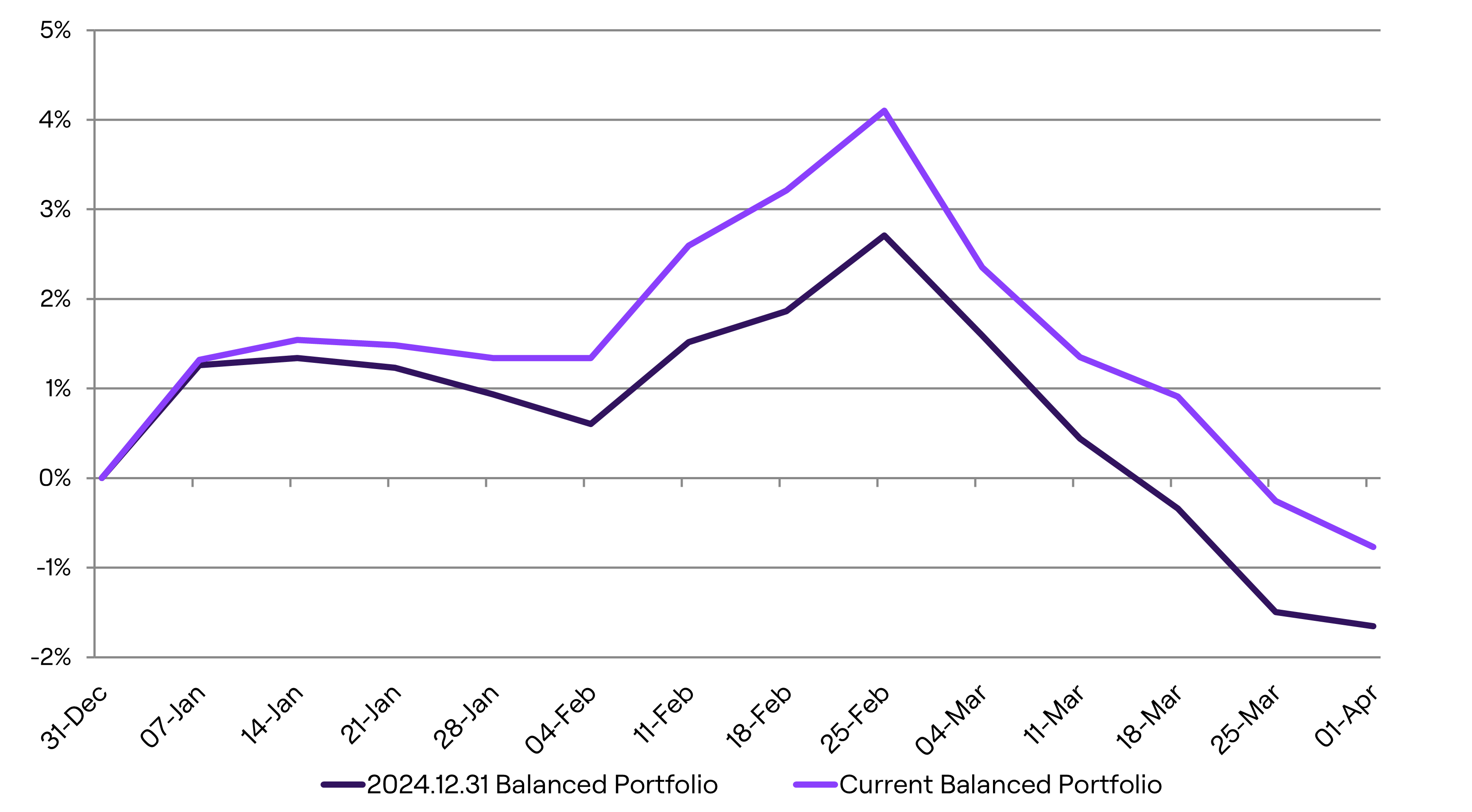

Against this backdrop, we have been pleased with how portfolios have performed. The changes we made at the end of January have allowed us to participate in the early strength in markets while also providing a degree of resilience through the subsequent volatility. This has resulted in meaningful outperformance during what has been a challenging period, as the chart in this report illustrates.

For now, we are broadly sticking to our knitting. Reacting too aggressively to short-term developments is rarely rewarded, and the instinct to do something – anything – in the face of uncertainty is one of the most common and costly mistakes investors make. That said, we are equally mindful that a prolonged period of elevated energy prices and geopolitical tension would have broader implications, and we remain alert to the need to adapt. There are avenues through which portfolios could be adjusted – increased exposure to areas that may benefit from higher energy prices, for example – though at this stage these remain considerations rather than actions.

The broader point is that we are operating in a world that continues to change. Geopolitics, energy security and economic policy are becoming more closely intertwined, and markets are reflecting that reality. It makes for a more complex environment, but not necessarily a less investable one. As ever, our focus remains on building and maintaining portfolios that are diversified, understandable and aligned with our clients’ long-term objectives.

Markets may be under pressure, and the headlines may at times feel unsettling, but as Neil Young reminds us, it is often worth keeping a sense of perspective. They are, after all, only castles burning.

Market Update

By Holly Warburton

Following Mark’s update and given the prevalence of news headlines over the quarter, there has been little chance of missing the key event, the US-Iran conflict, over the period. The overview below provides an update on what this has meant for underlying investment markets, both geographically and by sector.

Whilst it was a period of two halves with a strong January and February, overall, perhaps unsurprisingly from an asset class perspective, it was marginally negative across the board post-March. Global equities returned on average -1.6% and global bonds -0.2%, providing some protection, but given the potential long-term implications for inflation and subsequently likely interest rate hikes, not as much as you would hope in times of equity market stress.

Regionally, both the UK and emerging markets (“EM”) remained positive over the period returning +3.4% and +1.8% respectively. They both started the year strongly following a continuation of trends seen last year, namely a rotation away from the US and reinvestment back into “domestic” markets. This was swiftly reversed from 28th February, with deemed ‘higher risk’ regions across EM selling off, down -11.4%. Equally, alongside the UK to some extent, they also faced pressure as a key importer of now more expensive energy, as the oil price spiked over supply concerns. The US was the laggard at -2.7%, however the movements were opposite to the above, as the pre-conflict period captured much of the negative returns with relative strength experienced post. The US struggled in light of a strong re-pricing across key sectors over the first two months. While spending on AI infrastructure continued to attract capital, parts of software and information services were hit as investors began reassessing software valuations, fearing that AI-native tools, such as Anthropic’s Claude, could impact the business models of traditional software as a service (“SaaS”) companies.

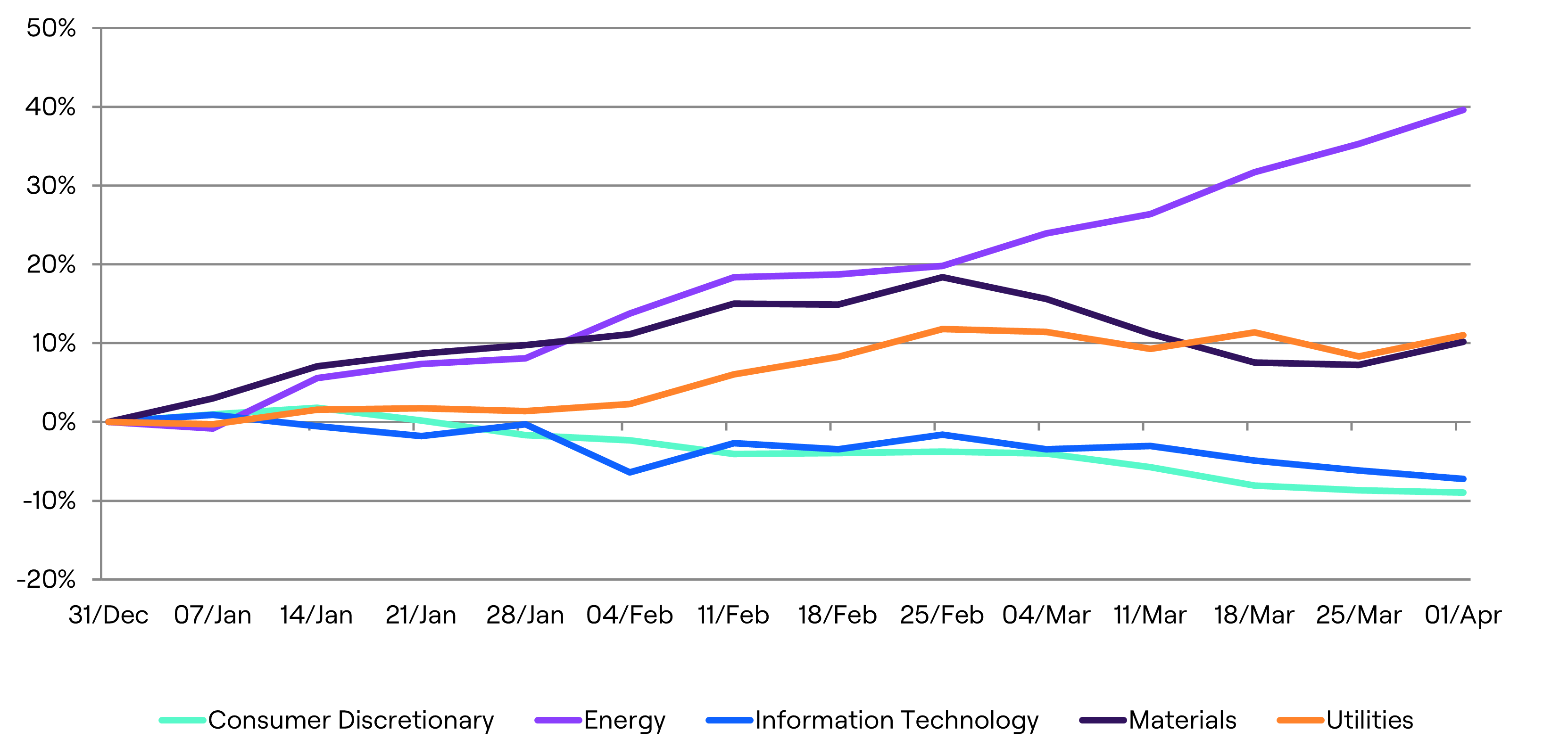

Continuing by sector (as charted below), energy was the clear standout, with global supermajors benefiting from rapidly rising oil prices. Similarly, materials benefited as investors sought exposure to physical commodities and minerals. Finally, the defensive nature of utilities came to the forefront and was boosted by increasing electricity demand required to power the ongoing expansion of AI data centres. Conversely, the sectors that dominated 2025 faced a valuation reset, predominately technology, which was heavily impacted as above. On the consumer side, discretionary struggled, considering rising energy prices and the impact this may have on household purchasing power, impacting major retailers and automotive manufacturers alike.

Finally, fixed income markets, although less impacted, also proved to be a volatile environment for investors as early-year optimism in the form of expectations for lower interest rates shifted toward defensive positioning. The energy spike reignited global inflation concerns, leading central banks like the Federal Reserve to maintain a “higher for longer” stance on interest rates.

As a result, government bond yields rose sharply, which created downward pressure on traditional bond prices. Certain areas showed resilience, corporate bonds for example remained relatively stable, supported by healthy company earnings despite the broader market swings.

Multi-Manager/Asset Strategies

By Bob Tannahill

This year has something of a sense of déjà vu about it.

Once again, we find ourselves starting the year with Trump having taken an issue that we all knew about (trade imbalances in 2025, now Iran in 2026) and taken it further than anyone assumed a rational person would.

By doing so, he has knocked out a pillar of the global economic system – in this case, safe access for shipping to the Persian Gulf – and by doing so he has left us all guessing as to whether the system will hold and where the worst of the damage will show up.

As I write, thankfully events seem to be cooling down. However, this latest drama looks increasingly like just one element of a broader pattern, as the world shifts from a US-dominated, post-Second World War global order to a new and more unpredictable multi-polar world. As investors, we believe that it is more important to get the big picture trends roughly right, than it is to try to get the micro trends exactly right. As we stand today, this shift to a fracturing and more inflationary world increasingly looks like the key issue.

In your portfolios this has been a focus of ours for the last few years. Over 2025, we fundamentally redesigned the core framework on which we build our equity allocations. Moving from a global core with thematic satellite positions to a regional core. We haven’t made a change as fundamental as this for more than a decade, and it is not something we did lightly. This major shift was driven by a view that regions mattered again, in a way they hadn’t been for many years, and this change was designed to bring a number of benefits:

- Reduced exposure to US equities and the US dollar, increasing geographic diversification;

- Greater ability for us to flex the regional positioning in portfolios; and

- At the margins, adding to sectors like energy, materials and defence.

One interesting feature of this shift has been the strength we have seen in our infrastructure and energy transition positions. The increased market focus on physical bottlenecks can be seen very clearly in our Global Solutions strategy. After a solid 2025, +11.1% (1), the fund is again benefiting from these trends in 2026 and is in positive territory at the quarter end.

This structural change, along with our usual management processes, is designed to help your portfolios better navigate this type of environment. An unexpected consequence of the current conflict is that it has provided a live stress test for these changes. While the dynamics are different, it is good to see the portfolios better capturing the upswings in markets without an associated increase in drawdowns in March - as the earlier chart in this update nicely illustrates. The net result is that our regional core portfolios have outperformed the global core portfolios by a healthy margin this year, more than 1% for the bellwether balanced strategy.

This work is an ongoing process, at times akin to painting the Forth Bridge, and our work on this subject continues. It is pleasing however to see the work that has gone into the portfolio redesign bearing fruit in the form of better results for you, our clients.

Please find performance commentary on our core multi-manager strategies below; Cautious, Higher Income, Balanced, Growth and Global Solutions, followed by our direct equity approach, Global Blue Chip. Each strategy is available via a segregated investment portfolio or via our Titan Global Fund Range.

If you would like to discuss any of our investment solutions further, please don’t hesitate to get in touch with a member of the team.

Cautious Portfolios

Lower Risk

Our Cautious portfolio returned +0.2% (2) ahead of both the UK and international peer groups, which posted -0.9% (3) and -0.3% (4) respectively.

January and February kicked the year off on a constructive note as financial markets continued where 2025 had concluded – steadily climbing as investors digested the shifting policy announcements of the Trump administration. The benign market environment abruptly ended at the end of February as strikes by a joint US-Israeli offensive against Iran turned markets on their head and a spike in volatility ensued.

There was nowhere to hide in March with risk assets broadly selling off across the board, most notably in gold and silver markets, which had witnessed significant returns in 2025, and emerging markets which had been previously buoyed by returns in Korean and Chinese bourses. Energy and certain commodity markets were certainly the outliers, where difficulties surrounding safe passage of container ships through the Strait of Hormuz caused prices in affected markets to spike due to shortage fears.

In a difficult quarter for equities, returns for the portfolio’s underlying holdings were mixed. Though largely positive, NinetyOne Global Quality Dividend Growth was the laggard, falling 3.4% over the quarter. Guinness Global Equity Income was the other negative holding, contracting 0.50%. KBI Global Infrastructure led the performance charts, returning 7.6%, while Pacific North of South EM Equity Income was also positive, up 6.1% over the period, after losing 10.4% of the fund’s NAV in March.

The portfolio’s fixed income allocation struggled to keep its head above water after the volatility across March, putting many holdings into negative territory for the quarter as investors pared their bets for the likely trajectory of interest rates. The portfolio’s core credit and subordinated financials holdings were principally the most impacted from the brutal sell-off, falling 3.3% and 3.8% respectively across March for a quarterly return of -1.8% and -1.2%.

Moreover, the portfolio’s diversifying assets bucket exhibited its value, producing solid uncorrelated returns. The Fermat Cat Bond Fund (+1.9%) and the Ruffer Total Return Fund (+1.4%) were in line with expectations and continue to prove their worth.

Higher Income Portfolios

Medium Risk

During a volatile period, our Higher Income portfolio behaved broadly as we would have hoped, with the capital value modestly down, leading to a flat total return (5) once you add back the quarterly dividend.

The quarter was divided into two segments: the run-up to the end of February, which was marked by strong markets, and March, which was weak on the back of the US attack on Iran.

Under the bonnet, our equities held up well with both Pacific and Schroder Dividend Maximiser finishing the quarter in positive territory, whilst Fidelity lagged. The latter was due to the European bias of the fund and the region’s perceived dependence on imported oil. Pacific was volatile over the quarter as emerging markets are also seen as oil dependent; however, it had such a strong January and February that even the March drawdown was not enough to put it into negative territory.

Bonds were mostly down but largely well behaved. Our most defensive fund, TwentyFour Asset Backed Securities, performed best and finished up +0.9%. On the other hand, GBP interest rates saw the sharpest correction over fears of an oil-induced inflation shock. As such it was not surprising to see our most UK rates exposed fund, Rathbone, being the weakest at -1.5%.

The investment trusts were volatile over the quarter, acting as a reminder that these tend to behave like equities on the downside. The only fund that stands out is the TwentyFour Income fund, which saw some weakness prior to the outbreak of the conflict. This was due to a busy new issue schedule for European collateralised loan obligations (loosely, blocks of corporate loans) combined with some nervousness about the debt of software companies as markets continue to feel out the full impact of generative AI. This is an area we are watching, however, for context the fund only finished the quarter down -2.5%, so the moves were not intolerably large.

Finally, our insurance-linked securities fund, Fermat, behaved admirably over the quarter, paying no attention to the gyrations of broader markets and finishing up 1.6%.

We made no changes over the quarter as the portfolio continues to behave in line with our expectations and, short term volatility aside, should continue to meet its objectives over time.

Balanced Portfolios

Medium Risk

Our Balanced portfolios returned -0.8% (6) slightly behind international peer groups, which posted -0.5% (7).

Amongst this volatile backdrop, we saw a disparity of returns from our underlying equity positions within Balanced portfolios. Despite pressures on the technology, Polar Artificial Intelligence continued its strong rally. We switched into this holding from our slightly more defensive Sanlam allocation in January. Within Polar alongside the key names, Nvidia and Alphabet, the fund focuses on the companies providing the infrastructure, the software and service providers integrating AI and businesses with proprietary data that can be leveraged to gain a competitive advantage. KBI Infrastructure was among the top performers benefiting from the gains across the utilities sector. Finally, despite headwinds in March, Pacific North of South EM Equity Income Opportunities finished the quarter +6.1%.

With respect to key detractors, the more growth-centric Brown Advisory Global Leaders struggled, finishing the quarter down 7%. Its largest sector allocations, technology and financials, were under pressure. Equally, Microsoft, Alphabet and Visa, which make up ~15% of the fund faced headwinds in the form of investor concerns over AI spending and potential delays on returns as well as Trump’s January 2026 proposal to impose caps on credit card interest rates and fees. BlueBox Technology and the S&P500 allocation was also impacted by similar trends.

Amongst our bond and diversifying positions there were no extremes to report as all holdings posted relatively flat returns and have performed at least in line with our expectations. Ruffer and Fermat were both positive, +1.8% and +1.4% respectively. Ruffer’s defensive mindset delivered attractive returns amid heightened geopolitical tensions. Fermat benefited from high embedded returns and a cautious approach to risk.

From an outlook perspective, we are comfortable with the underlying positioning and funds. The key question from here is how long the conflict lasts; if there is a relatively swift resolution, the economic fundamentals remain in place for a constructive year ahead.

Growth Portfolios

Higher Risk

Our Growth portfolios returned -0.5% (8) ahead of both the UK and international peer groups, which posted -1.7% (9) and -0.7% (10) respectively.

The first quarter of 2026 proved to be a tale of two distinct halves. The opening months saw strong dispersion in regional equity performance, supported by resilient fundamentals and positive investor sentiment. However, this strength reversed in the latter part of the quarter, as rising geopolitical tensions and policy uncertainty drove a broad-based retracement, leaving markets broadly flat overall.

In the first half, mega-cap technology companies came under increased scrutiny during the fourth-quarter earnings season, while attention also turned back to trade policy following a US Supreme Court ruling against the use of the International Economic Emergency Powers Act to justify “reciprocal” tariffs. In contrast, the second half of the quarter was dominated by a sharp escalation in geopolitical tensions. Following US military action against Iran at the end of February, March saw a significant intensification of hostilities, including coordinated strikes on strategic sites as part of “Operation Epic Fury” and the reported killing of Iran’s Supreme Leader, Ayatollah Ali Khamenei.

This shift in the geopolitical backdrop triggered a rapid deterioration in market sentiment. Investors reassessed risk, inflation expectations and the global growth outlook, resulting in a broad-based sell-off across most asset classes.

Global equities declined by -1.7% over the quarter. In contrast, regional markets provided some resilience: UK and Japanese equities each advanced by 3.4%, while emerging markets also delivered positive returns of 1.8%.

Within the Global Growth strategy, core exposures to artificial intelligence and infrastructure performed strongly. Polar Capital Artificial Intelligence returned 13.4%, while Atlas Global Infrastructure gained 13.2%, benefiting from increased energy demand and volatility linked to the US–Iran crisis, alongside its exposure to utilities and renewables. Emerging market exposure also contributed positively, with Pacific North of South EM Equity Income Opportunities advancing 6.1%.

On the downside, managers with a greater value tilt experienced more pronounced declines relative to sector-specific gains. Brown Advisory Global Leaders fell by -7%, which was disappointing given the broader market decline of -1.7%. Elsewhere, BlueBox Technology and the Vanguard S&P 500 fund posted more modest losses of -2.8% and -2.4%, respectively.

Despite heightened geopolitical tensions and increased volatility in the latter half of the quarter, the Global Growth strategy proved relatively resilient, declining only modestly overall. While uncertainty remains elevated, the outlook will depend on how the geopolitical situation evolves. The strategy remains well positioned to navigate near-term volatility while maintaining exposure to a potential recovery.

Global Solutions Portfolios

Higher Risk

Our Global Solutions portfolio returned +2.4% (11) ahead of international peer groups, which posted -0.9% (12).

A key feature of the quarter was a broadening of market returns. After a prolonged period of dominance by US mega-cap technology stocks, leadership rotated toward Europe, UK and emerging markets. Cyclical sectors such as energy, industrials and materials outperformed, supported by rising capital expenditure and improving economic data while technology returns were negative. Financials and healthcare stocks also struggled over the period.

Whilst emerging markets were the worst hit in March due to their reliance on now more expensive energy imports, over the quarter they still maintained positive momentum. Within the fund, strategies focused on structural growth themes across developing economies continued to perform well, particularly those exposed to environmental solutions, infrastructure development and technological adoption. Investor sentiment toward these regions has improved as earnings resilience and long-term growth potential become increasingly recognised.

The resource scarcity theme was a key contributor through the quarter. Strength in commodities alongside continued investment in artificial intelligence infrastructure supported companies exposed to advanced materials, automation and semiconductor equipment. Demand linked to data centre expansion and electrification trends continued to drive earnings upgrades across these areas. Robeco Smart Materials returned 18% over Q1 2026 and Polar Artificial Intelligence, which was brought in during the quarter to replace Landseer Artificial Intelligence, returned 13%.

Energy transition funds benefited from similar tailwinds; Polar Smart Energy was the top performer in this theme. The fund returned 14% as it benefited from sitting in the sweet spot of three of the market’s most powerful forces right now: AI, electrification and semiconductors. What looks like a clean energy fund is actually a picks-and-shovels play on rising power demand. The portfolio has exposure to the components, grid infrastructure and power electronics required to support an increasingly electrified and AI-driven economy. KBI Sustainable Infrastructure and Atlas Infrastructure also performed well over this period, returning double digits.

Looking ahead, the outlook for the portfolio’s core themes remains constructive. While short-term market dynamics may continue to shift, the structural drivers underpinning artificial intelligence, resource scarcity and energy transition remain firmly in place providing a strong foundation for long-term growth.

Global Blue Chip Portfolios

Equity Risk

By Ben Byrom

The Global Blue Chip strategy delivered a positive return of 1.9% (13) over the first quarter, ahead of the MSCI World’s -1.5% (14), outperforming by roughly 3.4%.

The quarter was defined by two overlapping market regimes. The first was a sharp re-pricing inside technology and software, as investors became more selective about where artificial intelligence would create value and where it might erode it. Heavy spending on AI infrastructure continued to attract capital, but parts of software and information services were hit by what the market increasingly treated as a “software as a service apocalypse”, particularly after new Anthropic tools intensified fears that some knowledge-based software models could face disruption. The second regime was geopolitical. As the Iran war developed through the quarter, energy markets tightened sharply and investors found themselves repositioning for a potential energy shock. Despite this threat, broader equity volatility remained more contained than might normally be expected, helped in part by repeated postings from President Trump on his Truth Social site that de-escalation remained possible. That steadier tone prevented a full risk unwind, but investors have become much more discriminating about what they are prepared to own.

Contributors

Performance was led by the portfolio’s exposure to energy, materials and selected industrial names. Exxon Mobil was a major contributor as record production volumes met a powerful sector tailwind from higher oil prices. Glencore also helped, supported by strength in copper and improving production, and whilst copper has fallen in reaction to events unfolding in the Middle East, its sizable coal exposure has been a beneficiary. Baker Hughes benefited from the growing link between the AI buildout and power demand, where data centre investment is now feeding through into demand for turbines, equipment and energy services. European utilities, including RWE, also added value as investors gave greater weight to energy security and long-duration power infrastructure. Agnico Eagle benefited from a historic run-up in gold prices as the ‘currency debasement’ trade collided with leverage. The correction that ensued was swift, deep and painful. Yet, such was the strength of the run, gold miners still posted very good returns for the quarter. With a lot of leverage now out, fundamentals can reassert themselves and we doubt the allure of hard assets in today’s environment has been dulled, although sentiment may need time to repair.

Detractors

On the other side of the ledger, the main detractors sat where the market was least willing to give companies the benefit of the doubt. Microsoft and Meta weakened as investors questioned whether very large AI-related capital expenditure would convert quickly enough into revenue and profit. Accenture and RELX were caught in the software and information services de-rating as investors reassessed the risk that AI tools could replace their product offering, or at the very least change their pricing model and addressable market. Unilever was also weak into quarter-end, with the shares falling sharply on 31st March after the announced merger of its food business with McCormick raised concerns over deal structure, timing and execution.

In broad terms, the quarter rewarded asset-heavy, cash-generative businesses with exposure to energy, resources and infrastructure, while penalising those parts of the market where valuation depended on distant growth or where AI threatened to change the profit mix more quickly than expected.

Key transactions

Trading activity reflected both that change in market leadership and our willingness to recycle capital into areas where the risk-reward had improved. We exited RELX and Adobe after the software sell-off deepened, not because we had lost conviction in the quality of the businesses, but because the market had started to treat large parts of the sector indiscriminately and price action had turned unhelpful. We also sold AMD, MercadoLibre, and Eli Lilly, each for slightly different reasons: in AMD’s case we felt upside might remain delayed and we wanted to change our AI Infrastructure mix; in MercadoLibre the market was becoming more focused on margin pressure as investments were made in the face of stiffening competition; and in Eli Lilly we chose to crystallise gains as competition is set to rise within obesity, one of its core markets.

Capital was redeployed into names more aligned with the quarter’s emerging opportunity set. Oracle was repurchased after strong results reinforced the idea that not all AI exposure is equal. Oracle’s data centre buildout, contracted backlog and improving revenue visibility made the set-up much more attractive after a steep share-price correction. We also added back Mosaic, again after a steep correction, as fertiliser markets look set to tighten as a result of the war-driven disruption on the Strait of Hormuz, and where the company offered operational leverage to potentially higher nutrient prices. New positions in Palantir, Cameco and Pan American Silver reflected our preferences for practical AI deployment, fuel security – we think nuclear has a real shot of becoming the must-have fuel source of the future - and scarce real assets as silver’s supply versus demand deficit continues to grow.

The thread that links these transactions together is in keeping with our new approach (see our Q4 Insights) where we are more willing to remove stocks that are acting against our performance interests whilst aligning ourselves with holdings whose profit pools are shifting in a way that is under appreciated by the market and are likely to surprise to the upside in time.

We enter Q2 2026 with a portfolio that is focused on structural growth, but with greater respect for a world in which energy, inflation and geopolitics are again moving markets. The key question now is whether the Iran war cools or broadens. A sustained easing would help rates and long-duration assets stabilise; a prolonged disruption in energy would risk higher inflation, higher bond yields and renewed pressure on richly valued equities and private credit markets ahead of the US mid-term run-in. For now, we remain focused on businesses with clear earnings visibility, strategic relevance and improved pricing power.

Fund in Focus

RWE

By Alex Rich

RWE is not the sort of stock that typically earns a Stock in Focus badge, and yet we own it in the Titan Global Blue Chip strategy (the “Strategy”). It may lack the perceived relevance of oil or gold plays, the narrative elasticity of luxury, and the glamorous allure of anything with “AI” in the title, but what it does do, it does well.

It generates electricity. Reliable, yet seemingly dull. Though, as we’ll discover throughout, this is a crucial company despite its perceived ambiguity.

In a world increasingly defined by energy insecurity, geopolitical friction and the quiet but relentless expansion of power demand, dull has become indispensable. If markets have spent the past few years obsessing over the front end of innovation and getting a chatbot to simultaneously write a recipe and figure out what that wart is, RWE sits firmly at the back end determining whether there’s electricity to power those queries in the first place.

RWE is a German energy major with a deliberately balanced dual model, renewables for growth and flexible gas generation for stability. Renewable capacity provides structural upside as Europe and the US decarbonise, while dispatchable gas assets allow RWE to monetise volatility and assist in times of need, an increasingly valuable trait in fragmented energy markets (especially in Europe, which isn’t blessed with natural resources). The company’s development pipeline is substantial, with over 30 potential sites across Europe offering more than 3GW of grid-connected infrastructure suitable for data centres. And capital allocation reflects similar ambition, with RWE planning to invest €35bn between 2026 and 2031 to reach 65GW of capacity, with nearly half directed towards the US, where electricity demand growth is both clearer and less encumbered by policy inertia.

Where RWE becomes more interesting, if not quite exciting, is its role in powering the next phase of technological expansion. Electrification across transport, heating and industry is already lifting baseline demand, but the real inflection comes from data centres and AI. Training models, running inference, and scaling digital infrastructure are energy-intensive activities and RWE is positioning accordingly. Around 80% of its power purchase agreements are now driven by data centres, and its extended agreement with ASML underscores its relevance to the semiconductor supply chain. In effect, while Nvidia sells the picks and shovels, RWE is supplying the electricity required to use them, and its US build-out (spanning solar, wind, batteries, and eventually flexible gas) aligns neatly with enabling the fund’s technology and innovation theme.

Equally, RWE sits at the intersection of a second theme, energy localisation and security – aligning well with the fund’s changing world theme. The past two years have been a reminder that global energy markets are both economic systems and indeed political ones. Events involving Iran and Venezuela have demonstrated how quickly supply and power dynamics can shift respectively, with the very recent ceasefire-driven price moves underscoring just how fragile sentiment remains. Against this backdrop, RWE’s investments in Germany can be viewed through the lens of resilience, something that the world is expected to need more of as we enter a more nationalistic era. The expected tender of 12GW of new gas capacity in Germany highlights a broader recognition, particularly within Europe, that intermittent renewables require firm backup and energy independence is increasingly non-negotiable.

The market appears to have noticed the above, and RWE shares are up ~30% in Q1 2026, supported by improving fundamentals and deal-making, a series of positive broker revisions, and a generally supportive macro backdrop as discussed. RWE offers exposure to two structurally durable sub-themes with the fund (electrification and energy security) without relying on heroic assumptions. It is capital intensive, yes, and politically exposed, inevitably, but it is also embedded in the physical infrastructure of the modern economy in a way few companies are. So in a stock market increasingly populated by intangible assets and optimistic narratives, there is a certain logic in owning the company that keeps everything else running.

Data sources:

- Titan Global Solutions O Acc, GBP Total Return 31/12/2024 to 31/12/2025. Source: FEfundinfo.

- GBP Titan Cautious Model Performance Data, Total Return 31/12/2025 to 31/03/2026. Source: Titan Wealth (CI) Limited.

- Investment Association (“IA”) Mixed Investment 0-35% Shares Sector, GBP Total Return 31/12/2025 to 31/03/2026. Source: FE fundinfo.

- Asset Risk Consultants Sterling Cautious Private Client Index, GBP Total Return 31/12/2025 to 31/03/2026. Source: FE fundinfo.

- GBP Titan Higher Income Model Performance Data, Total Return 31/12/2025 to 31/03/2026. Source: Titan Wealth (CI) Limited.

- GBP Titan Balanced Model Performance Data, Total Return 31/12/2025 to 31/03/2026. Source: FE fundinfo.

- Asset Risk Consultants Sterling Balanced Asset Private Client Index, GBP Total Return 31/12/2025 to 31/03/2026. Source: FE fundinfo.

- GBP Titan Growth Model Performance Data, Total Return 31/12/2025 to 31/03/2026. Source: FE fundinfo.

- Investment Association (“IA”) Mixed Investment 40-85% Shares Sector, GBP Total Return 31/12/2025 to 31/03/2026. Source: FE fundinfo.

- Asset Risk Consultants Steady Growth Asset Private Client Index, GBP Total Return 31/12/2025 to 31/03/2026. Source: FE fundinfo.

- GBP Titan Global Solutions Performance Data, Total Return 31/12/2025 to 31/03/2026. Source: Titan Wealth (CI) Limited.

- Asset Risk Consultants Equity Risk Asset Private Client Index, GBP Total Return 31/12/2025 to 31/03/2026. Source: FE fundinfo.

- GBP Global Blue Chip Performance Data, Total Return 31/12/2025 to 31/03/2026. Source: Titan Wealth (CI) Limited.

- MSCI World, GBP Total Return 31/12/2025 to 31/03/2026. Source: FE fundinfo.

All performance data above was collated on 13/04/2026.