Building resilience in a changing world

Investors have found themselves in a world that looks familiar but where the rules and customs they have been accustomed to no longer apply in the same way. The investment landscape has shifted, as the perceived investment norms are facing growing challenge and disruption. We are no longer debating whether the transition is real and we are certainly not preparing for a return to the world we once knew. Instead, a different set of questions now dominate: what needs to be reorientated, brought home and rebuilt, when should this be done and how will it be financed?

Michael Every (1), geopolitical strategist at Rabobank, has been good at framing the broader shift that is underway, especially under Trump 2.0, from one of global trade toward statecraft: a world in which trade, money, technology, industrial capacity and security are no longer separable spheres, but levers to be pulled in pursuit of national objectives. States are increasingly asking not what is most efficient in a frictionless global system, but what is necessary in a contested one. In such a world, alliances endure only for as long as interests remain aligned – look no further than the recent announcement from the UAE on their OPEC membership. What works for us today may not work for us tomorrow. This creates an uncertain setup.

America has become the Petri dish, where the Trump administration is attempting, in the words of Michael Every, a reverse perestroika – turning decades' worth of GDP created by consumption into GDP generated from state-driven industrial policy. It’s a high-stakes gamble that aims to turn the tables on China, a country whose ascent into the World Trade Organisation has benefitted from the West’s willingness to outsource. This sent it on a trajectory that would eventually end up with it challenging the US’s status as global hegemon. That challenge has been brewing for the best part of a decade and is now in full swing. The kinetic wars in Ukraine and now the Middle East are symptoms of this power struggle, flare-ups within a broader dynamic that has the potential to change the world order as we know it and rewire the way it works – in some respects the stakes could not be higher.

Mapping out what a country or regional bloc may need for it to become more resilient will align us with the investments that should be made. Aligning ourselves with these flows will be critical in keeping us on the right side of opportunity.

The following is not an exhaustive list of ‘must-haves’ but areas where we see capital heading (and expect it to continue to head) in a sufficiently measurable way that qualifies them as an investable sub-theme, fitting our resilience roadmap.

Energy security

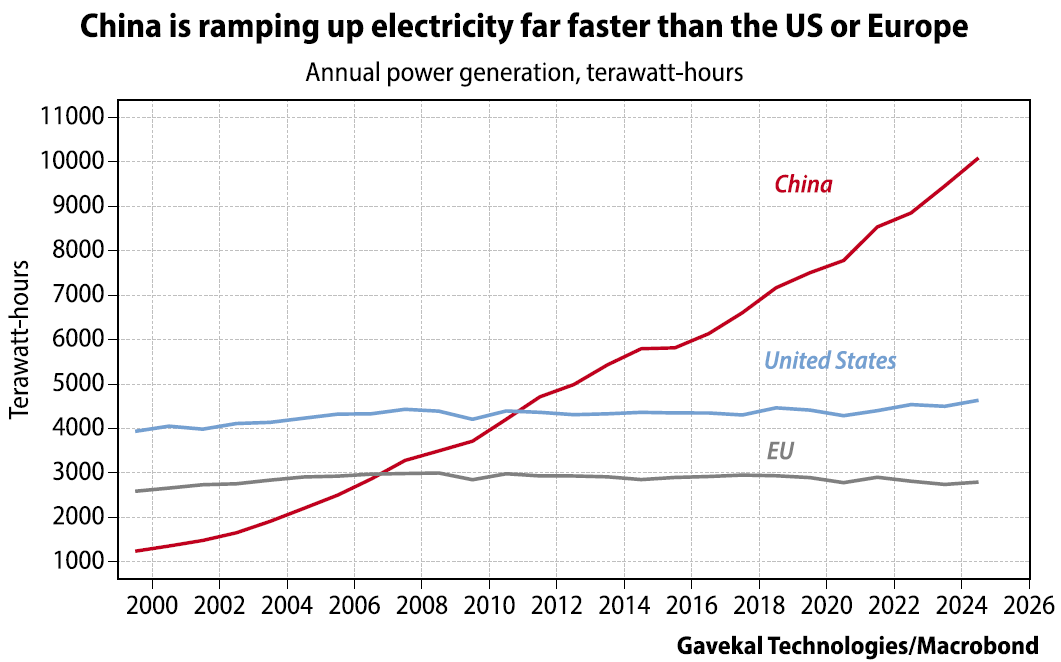

Energy security sits at the centre of our resilience map. To grow requires energy. To thrive requires energy abundance. To generate abundant energy, we need access not just to hydrocarbons, but to energy systems that are affordable, reliable and robust enough to support the modern-day needs and objectives of electrification, data centres, industrial output and military readiness. The International Energy Agency now expects electricity demand from data centres alone to more than double by 2030, to around 945 TWh, with AI the main driver of that increase. China got the memo long before the West realised why.

Even the European Commission has started to increase the deployment of capital to better prepare its grids, with some €1.2 trillion earmarked for distribution and transmission by 2040. In the resilience agenda energy security isn’t about securing access to oil and gas, nuclear or even building out your renewable energy assets, it is also building the system around it.

A power surge is underway, leading sustained demand for power generation in all forms, including nuclear, and demand for grid infrastructure equipment such as cables, power lines, transformers, switchgear, interconnectors, backup power generators, storage and power-management software to grow as power grids get a much-needed makeover to bring them up to spec to deal with the demands of the new era.

As an example, Europe has leaned heavily into renewable generation, but much of the network was not designed for intermittency, congestion management or a sharp rise in electricity intensity. These vulnerabilities undermine the resilience of everything that feeds off the grid. Mapping out these vulnerabilities shows the spending pathway that gives confidence in an investment thesis that grows as the demand curve steepens.

The same logic applies to other areas of scarcity, whether through geographical or geological fortune and an overreliance, whether through policy choice or need, on just-in-time supply chains that are centred in regions that may choose, one day, not to be so generous.

Raw materials and finished products

For years the West treated access to copper, rare earths, steel and aluminium as an outsourcing problem. Today, these are a sovereignty issue, and action is now being taken to address the vulnerabilities that have built up in the system.

Whilst mining is important, it is largely dependent on how blessed a region is with the ‘right’ geology. That said, refining the raw material into a useful product is as crucial and can be done anywhere. However, the midstream processing value chain is a dirty, energy-intensive business and during the 2000s and 2010s the West decided it didn’t need to do these activities, as it could outsource them to other countries that were willing to build that capability. That seemed the logical route to take in an era of global supply chains that had become so finely tuned they were adept at providing product on demand at very attractive prices.

As the West enjoyed the benefits (price and environmental), it turned a blind eye to the strategic vulnerabilities growing beneath the surface. Today, China dominates rare-earth separation and processing, especially in heavy rare earths, while also remaining the world’s largest copper refiner (2). China has effectively created the choke-point that will allow it to dictate who gets to participate in the modern economy.

Understanding the implications of this vulnerability has prompted the Trump administration to undertake a number of initiatives to address it, including investment, funding, regulatory policy and price floors to incentivise private investment.

One example is the $1.6bn financing package that was put together for USA Rare Earth, a domestic company developing America’s only heavy rare earth mine. Other examples of strategic deals between government and industry include investments in MP Materials (a light rare earth producer), Vulcan Minerals (a magnet start-up), Trilogy Metals (copper and zinc miner in Alaska), and Lithium Americas (a lithium miner).

The US government has launched a $12 billion critical minerals stockpile, known as Project Vault. It aims to maintain a 60-day supply of essential materials for industry, including rare earth elements, battery inputs, semiconductor materials and other key resources for energy and industrial production.

Commodity supply chains cannot be built quickly, especially in the US where decades of regulation and NIMBYism slowed the process to, on average, 29 years to develop a new mine, as per an estimate by S&P Global, while new primary copper mines that entered production globally between 2019 and 2022 took an average of 23 years from discovery to commercial production. That is too slow in a world that increasingly sees materials security as a strategic imperative. Again, the Trump administration is seeking to fast-track selected mining projects in an effort to reduce dependence on foreign supply and accelerate domestic production.

Even Europe, often seen as cheerleaders of the clean economy, is attempting to change tack with the European Critical Raw Materials Act (CRMA), which shifts EU policy from market-dependent sourcing to a more self-sufficient route. It sets out 2030 supply targets across the value chain, aiming to achieve 10% of current resource needs from domestic extraction (prior to the CRMA domestic extraction was ~3%), 40% from processing (~20% concentrated in a few metals) and 25% from recycling of strategic materials (<1% for most strategic metals). Additionally, the legislation aims to limit reliance on any single third country, requiring that no more than 65% of any strategic raw material originates from a single non-EU country at any stage of the value chain . This law (passed in 2022) acknowledges a strategic vulnerability, underscoring the urgency to create redundancy, diversify supply and build some form of strategic insurance. Despite the positive step in legislation, progress has been slow, hampered by regulatory barriers.

Defence

This sector demonstrates how old habits and doctrines are giving way as governments reassess threats, technology and the economics of the modern battlefield. The old debate on whether the West should spend more on defence has largely been answered. NATO allies have pledged to commit up to 5% of GDP annually on defence and defence-related security by 2035, while the US has proposed lifting its own defence budget to $1.5 trillion for fiscal 2027, up from a projected $901 billion expected to be spent in 2026. We are already starting to see money move, as the European Defence Agency estimates that EU member state defence spending has risen to around €381 billion in 2025, taking the bloc to roughly 2.1% of GDP, above the old 2% NATO threshold (4).

The more important questions now are what the actual magnitude will be – beyond the promise and incremental raise to-date, and how that money will be spent. For decades, Western military superiority was built around a small number of large, expensive and technologically advanced platforms. Those systems will remain important, but their dominance is being challenged by cheaper, expendable capabilities that can be produced faster and in far greater numbers. One reason we sold some of our defence exposure (BAE Systems and Lockheed Martin) recently was this growing asymmetry: the marginal budget dollar is no longer guaranteed to flow to the most exquisite legacy platform. It may instead flow toward lower-cost solutions and the industrial base needed to manufacture at scale.

This shift is already visible. Through necessity, Ukraine has changed the battlefield economics. Such is their success, Gulf states are now procuring Ukrainian interceptor drones costing a fraction of the Patriot interceptors that can cost up to $4 million a shot. That kind of exchange ratio is not sustainable in a world of mass-produced drone swarms and persistent, low-cost attack systems. These lessons are now permeating across Europe’s five biggest military powers, who are now working on a joint programme to bring low-cost air-defence systems, such as autonomous drones or missiles, into production. Resilience in defence therefore runs not only through the headline primes, but through the broader ecosystem of autonomy, sensors, jamming, propulsion, power systems and scalable production that modern warfare increasingly demands.

Artificial Intelligence

AI belongs as much within the resilience framework as it does technology and innovation. To fall behind in AI is to fall behind in industrial productivity, cyber capability, military decision-making and, ultimately, national competitiveness. It is considered so important, it is now a matter of state policy. In November 2025, the White House launched the Genesis Mission, a federal initiative designed to use AI to accelerate scientific discovery by linking supercomputing, federal datasets and advanced research infrastructure. The emphasis on energy, national security, semiconductors and critical materials all sit close to the heart of the state agenda.

The US government’s growing willingness to intervene more directly in strategic industries reinforces the importance of it all. Intel was one of Washington’s first interventions, after taking roughly a 10% stake in the company by converting future CHIPS Act-related grant funding into equity. Whether that becomes a template for wider intervention within the semiconductor industry remains to be seen, but the boundaries between state-driven policy, capital allocation and industries with a strategic importance are becoming less defined in today’s world of ‘statecraft’.

If governments believe not having cutting edge access to AI leaves them vulnerable, then think what that means to those who make it their business to be at the frontier of model development. The scale of private capital already being mobilised only accentuates the urgency from an industry perspective and it is accelerating, not slowing down, despite growing funding fears and a brewing private credit crisis. Alphabet increased CapEx by +140% year-over-year and Oracle +100%, Microsoft by 82%, Meta 75%, Combined, US CapEx in AI contributes roughly 1% to GDP becoming a meaningful contributor to national growth.

Such is the scale, these once free cash flow rich machines are no longer able to cover it all with their free cash flow alone and Bank of America expects the ‘hyperscalers’ to issue around $175 billion of new debt in 2026 to fund their AI infrastructure build out, up sharply from prior expectations and well above recent annual issuance.

Within the resilience framework, the demand of AI extends well beyond chips, software and energy; it reaches into strategic industries, debt markets and the funding architecture itself.

Financing

This leads to a critical question: how does the West find the capital to reorient its economies without nationalising them outright? The answer, in our view, is that we are moving toward a more directed form of capitalism, one in which central banks, treasuries, regulators and private capital markets become increasingly aligned around strategic objectives. In an era of statecraft, genuinely independent monetary policy becomes harder to reconcile with broader national priorities. It points towards a period of financial repression: funding conditions kept easier than they might otherwise be, public tolerance for asset support when stability demands it, and a greater willingness to shape where savings and capital are directed. The release valve for this is likely to be inflation and, at times, currency weakness. In other words, the burden of adjustment is less likely to fall on higher real rates, but instead on a gradual erosion of money’s purchasing power.

We can already see the working drawings of the architecture being built. The European Union’s Savings and Investments Union is explicitly intended to create a financing ecosystem that benefits the EU’s strategic objectives while channelling household savings into productive investment.

Stablecoins

In the US, stablecoins are an intriguing addition to this story, offering a kind of reverse capital control for the United States. Put simply, stablecoins are digital currencies designed to maintain a fixed value, typically pegged to the US dollar and backed by reserves such as cash or short-term government bonds.

Traditional capital controls try to stop money leaving a system – although we argue above that governments may try and incentivise savers to redirect capital to where they would like it.

A dollar stablecoin regime could do almost the opposite by making it easier for offshore users, firms and savers to transact, settle and store value inside a dollar-based monetary ecosystem. Under the GENIUS Act, US payment stablecoins must be backed one-for-one by specified reserve assets, including short-dated Treasuries, certain deposits, reserve balances and closely related cash-like instruments, while issuers are also subject to anti-money-laundering and sanctions-compliance obligations. BIS research suggests that inflows into dollar-backed stablecoins would be sufficient to lower short-term Treasury bill yields.

That is why some commentators, such as Michael Every, and, more broadly, Bret Johnson, see stablecoins as potentially important to US economic statecraft. They infer stablecoins widen the global distribution of digital dollars while simultaneously deepening structural demand for T-bills. They become not just a means of payment but rather a part of the plumbing of US fiscal resilience. More than that, if even part of the opaque offshore dollar system migrates onto regulated, auditable, blockchain-based rails, Washington could gain greater visibility over some cross-border dollar activity and more leverage through compliance, sanctions enforcement and control of the regulated on-ramps and issuers. Whilst it would not amount to full control of the offshore dollar market, it could well extend US reach within it.

You will not make much from simply holding a US stablecoin, if anything at all. Under the GENIUS framework, payment stablecoins are intended to function as digital cash, not yield-bearing savings products, with issuers generally prohibited from paying interest or yield to holders. The ongoing fight is over whether rewards for certain activities can replicate the yield that would otherwise have been earned, and banks are understandably nervous that if those inducements become sufficiently attractive, they could pull deposits away from the traditional banking system – potentially destabilising it. Yet the momentum behind stablecoins is obvious. They offer a frictionless way to transfer value from one wallet to another, across borders and across time zones, with little of the legacy friction embedded in correspondent banking. If you have a phone or a computer, you can hold one, send one or receive one.

When money changes, the financial architecture around it eventually changes too. We have already seen how central banks responded to prior stresses in the financial plumbing: by flooding the system with liquidity, compressing yields and encouraging a relentless search for return. Much of that liquidity ended up supporting asset prices and weakening the purchasing power of money rather than restoring stability to a system that would offer a genuine store of value for savers. In an age of financial repression, that process may deepen. Funding conditions are likely to be kept easier than they otherwise would be, strategic assets may receive privileged treatment, and new monetary rails may emerge that serve very specific policy objectives.

Stablecoins, therefore, may become another mechanism through which the state influences the cost and direction of capital. Whilst this is another inference, there have been prior examples in history where states have bent their monetary system to achieve certain objectives.

For example, the Soviet Union had built a multi-tier system around the rouble to maintain total control over the economy. It operated with cash roubles that were used for wages and payment for consumer goods and a non-cash rouble used as an accounting unit used by state enterprises to pay each other. A transferable rouble was introduced to facilitate trade between the Soviet Union and its socialist allies in the CEMA. The system of several roubles crumbled under reform in the glasnost and perestroika years under Mikhail Gorbachev as unintended consequences led to financial chaos and hyperinflation.

Whilst we do not argue for a direct repeat, we are suggesting that once money becomes more openly political, it becomes harder to assume that one dollar, in every form and in every venue, will remain economically and politically identical to every other. Especially now a cryptocurrency technology exists that would, with relative ease, allow a multi-tier system with each layer having its own set of rules-of-use programmed into it. This is the rhyme worth paying attention to.

Desperation Capital

This leads to our final point, and that is desperation capital. By that we mean the way individuals respond when the ‘old’ social contract of incremental progress begins to break down – which arguably has been underway since the financial crisis and accelerated following the huge monetary response to Covid. The Organisation for Economic Co-operation and Development’s (OECD’s) latest wage bulletin says real wages remain below early-2021 levels in half of OECD countries, while the International Monetary Fund noted in January that the high cost of living remains the most important concern cited in US household surveys, combined with housing affordability remaining a structural problem across much of the developed world.

In this environment, it is not hard to see why more people are drawn toward asymmetric outcomes in financial and prediction markets, crypto and trading apps. Not necessarily because they are reckless, but because conventional ways of catching up increasingly feel closed to them. “Seeking escape velocity” is how we frame it, and we actually wrote in depth about this topic earlier in the year which you can read here. In summary, this is the rational response of individuals under strain. If traditional employment no longer offers a credible path to the life people are primed to expect under current social norms, it should come as little surprise that they turn to alternatives such as financial markets and investing serious time in developing the skills to navigate them. In a world where pay, promotion and security feel increasingly uncertain and dependent on decisions made by others, these pursuits offer something increasingly scarce: a sense of agency, tangibility and direct connection between effort and outcome.

Interestingly, the Chairman of BlackRock made similar thoughts in his annual letter but argues that the funding required to rebuild supply chains and reorientate the economy will be of such scale it will not just involve governments, banks, and institutions but the mobilisation of household savings. His argument is that the tokenising of assets, allowing retail investors to hold portfolios of investments in a digital wallet on their phone or computer, could eventually make investing as accessible as sending a payment – thereby broadening the pool of potential savers and quantum of capital that could be put towards strategic objectives. In this world, online broker platforms such as Coinbase, Robinhood, and Interactive Brokers (amongst others) become critical access points to ownership for the masses.

Put this together and the lens of resilience helps better frame the investment opportunities within a “changing world”. Capital is already flooding energy security, grid infrastructure, critical materials, defence electronics, drones, AI infrastructure, automation, robotics and space. Innovative solutions will capture value, while some legacy players will remain relevant and others may see capital shift elsewhere.

The areas discussed above are not an exhaustive list, but rather represent just some of the opportunities within our changing world theme. We manage our exposures to ensure we are not overly skewed to any one sector or product. Our construction is by design and the constraints we are seeing are real as ‘bytes meet atoms’. In other words, the rapidly expanding digital world is now meeting the limitations of the physical world, placing strain on a system, with the constraints and bottlenecks offering real investment opportunities as fiscal and monetary policy are put to work to alleviate them. It won’t go ‘straight up’, but we do believe these areas will offer growth for years to come.

Sources:

- https://www.macrovoices.com/podcast-transcripts/1500-michael-every-usd-stablecoins-in-the-age-of-economic-statecraft?utm_source=chatgpt.com "Michael Every: USD Stablecoins in The Age of Economic ..."

- https://www.csis.org/analysis/developing-rare-earth-processing-hubs-analytical-approach

- https://commission.europa.eu/topics/competitiveness/green-deal-industrial-plan/european-critical-raw-materials-act_en?utm_source=chatgpt.com "European Critical Raw Materials Act"

- https://eda.europa.eu/docs/default-source/brochures/2025-eda_defencedata_web.pdf