“When you see one cockroach, there are probably more.” Jamie Dimon, October 2025

The JP Morgan CEO made this comment regarding weaknesses in what is often called the “shadow banking” sector - the part of the financial system made up of non-bank lenders and investment vehicles that provide credit outside traditional banks - in a Q3 2025 earnings call. It was prompted by the collapse of First Brands, a US auto parts supplier, and Tricolor, a US subprime auto finance business, two very different businesses whose failures nevertheless raised wider concerns over lending standards and transparency in private credit and served as a warning to investors that further problems may yet emerge.

An area of the market that has historically been very popular among investors, particularly during periods of ultra-low interest rates, the sector is now beginning to fracture, leading to investor concern and a repricing of the asset class.

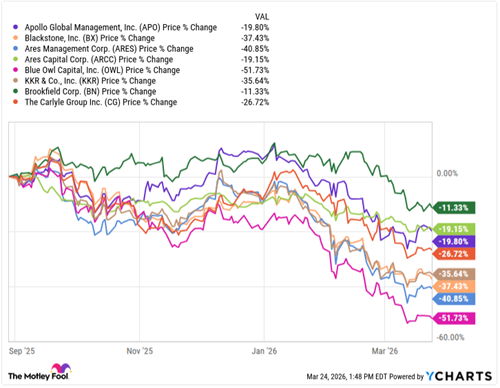

BlackStone Private Credit Fund (BCRED) recently made headlines for allowing investors to request the sale of a record 7.9% of shares in its flagship vehicle. As highlighted, other names in the space has also actioned the same. Oaktree Strategic Credit Fund (8.5%), Blue Owl Credit Income (5.2%) and Apollo Debt Solutions (11.2%) are among the larger fund vehicles that have experienced elevated redemption requests – meaning investors asking to withdraw their money from the fund – with performance also impacted by the decline in the value of their underlying investments.

Fig 1. Selective fund performance since end of Q3 2025

What started in late 2025 has accelerated into the first quarter of 2026 as private credit funds face a surge in redemption requests, forcing some fund managers to implement restrictions, although it should be noted that not all of the referenced funds have implemented redemption restrictions at the time of writing.

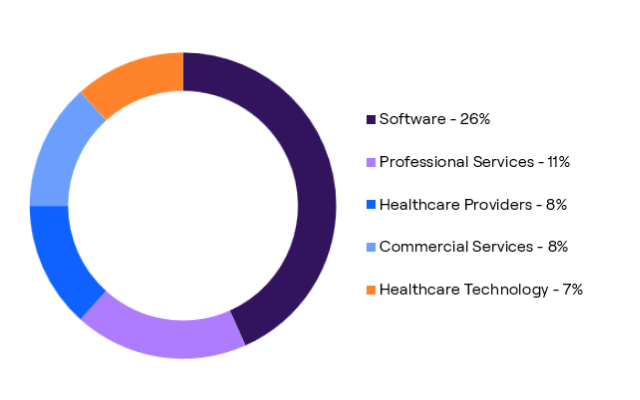

Default rates have been increasing, rising from an historic average of 2% per annum in the senior secured lending space, to 5% over the last 18 months. This indicates a build-up of stress in leveraged financing. The turmoil appears to be primarily concentrated on business development companies (‘BDCs’) and their exposure to the software sector. As seen in equity markets, software has faced weakening investor sentiment due to concerns surrounding the impact artificial intelligence (‘AI’) is likely to have on revenues, increasing the likelihood of defaults in the sector.

Private credit funds tend to avoid cyclical areas of the market due to long and illiquid investment timeframes, meaning fund managers do not want to be realising underlying investments when the economy could be in a cyclical downturn. For example, 16% of the leveraged finance market is in the energy sector, private credit has historically replaced that exposure with alternative industries, often favouring software.

Software represents roughly a quarter of BDCs exposure. However, that figure has come under increasing scrutiny with some commentators suggesting the true exposure may be higher and potentially understated by managers.

Many software loans within BDCs and private credit more broadly originated between 2019–2021, a period considered a high risk “vintage”. A “vintage” is the term given to the period when loans are originated. Different market environments, levels of interest rates, varying levels of covenants are some of the characteristics that affect the returns available on loans.

Software loans between 2019–2021 were characterised by aggressive investor demand searching for yield in an environment of high company valuations, loose covenants and low interest rates, while risks to business models associated with the arrival of AI have amplified those risks.

Moreover, returns are often predicated on enterprise values (‘EV’) and company cash flows. However, EVs are declining and cash flows are being reinvested into the company, leaving investors without income and instead reliant on payment in kind (‘PIK’) notes. The prevalence of PIK structures is often an indication of rising stress in the market.

Contrary to lending to software companies, asset-backed lending gives that added element of security through the underlying asset. As such, asset back-lenders haven’t observed the same level of repricing currently being inflicted on the BDC market overly exposed to software.

While private credit managers would argue the asset class is now attractively priced with widening spreads and better covenants, the recent stress highlights why selectivity remains crucial. Even where valuations appear more compelling, the events discussed above are a reminder that not all areas of private credit carry the same risks.

Titan Wealth does not have broad or comprehensive direct exposure to the parts of private credit currently under the greatest strain within our multi-asset fund range. However, we are highlighting these developments not because they are a direct issue for portfolios today, but because they are an important sign of where risk is emerging in markets and where investor caution is warranted.

Our Higher Income strategy invests in the Sequoia Economic Infrastructure Income Fund, which lends to projects including roads, bridges, ports, telecoms, utilities, power and renewable energy and, as such, has exposure to essential, asset-backed infrastructure rather than the more challenged areas outlined above. In our view, this provides a materially different risk profile to the software-heavy and more liquidity-sensitive parts of the private credit market currently under pressure.

In short, while we believe the current dislocation in parts of private credit is significant and worth monitoring closely, our positioning remains deliberate: where we do have exposure, it is targeted towards areas we believe are more defensive, more transparent and better aligned with long-term income generation.