Imagine asking 10 households to unpack their shopping bags onto the kitchen table. Some would be filled with children's snacks and packed-lunch essentials. Others might contain ingredients for dinner parties, pet food, garden supplies or enough coffee to keep a small office functioning. Most would look entirely different, which is precisely why inflation affects people differently.

Although inflation is reported as a single figure, the reality is that every household has its own spending habits, priorities and financial pressures. As a result, the rising cost of living isn't experienced in exactly the same way by everyone.

Official inflation figures only tell part of the story. In October 2022, UK inflation reached 11.1%, the highest level in more than four decades (1). While inflation has since fallen significantly, prices have not returned to where they were before. The result is that many households continue to feel the effects.

A family with growing children may notice rising supermarket bills first. Someone who commutes every day may feel every increase at the fuel pump. Retirees could be more focused on household energy costs, while frequent travellers might pay closer attention to the cost of flights and accommodation. The headline inflation figure remains the same, but the day-to-day experience often looks very different.

This can be even more pronounced in the Channel Islands. For residents of Jersey and Guernsey, the official inflation rate often bears little resemblance to how rising costs feel in everyday life. After all, life on an island comes with its own costs and considerations.

Housing provides a good example. Property prices and rental costs in both islands remain significantly higher than in many parts of the UK, with Jersey property prices exceeding London and more than double the UK average (2).

Many everyday goods must also travel a little further before reaching supermarket shelves, with transport and distribution costs often feeding through into retail prices. As a result, the cost of living in the Channel Islands can feel noticeably different from elsewhere in the British Isles. Recent analysis suggests that the overall cost of living in Jersey is at least 10% higher than in the UK. As a result, two households can experience inflation very differently.

That's why, particularly in the Channel Islands, inflation is not just a national statistic – it's a personal experience shaped by where you live, how you spend your money and the stage of life you are in.

Which brings us back to those shopping bags on the kitchen table. While inflation is reported as a single number, our lives are rarely average. This raises an interesting question: if no two households spend money in exactly the same way, how can a single inflation figure represent everyone?

What inflation actually measures

To answer that question, it helps to understand how inflation is calculated. The Office for National Statistics tracks the cost of a representative "basket" of goods and services intended to reflect typical consumer spending habits. The contents of this basket evolve over time. Recent additions have included items such as croissants, houmous and non-alcoholic beer, reflecting the way our spending patterns continue to change.

By tracking how the cost of this basket changes from year to year, economists can calculate the Consumer Prices Index (“CPI”), which is the measure of inflation most commonly reported in the headlines. It's a useful benchmark, but it's important to remember that it is still only an average. After all, very few households shop exactly like the “average” household.

This is sometimes referred to as your personal inflation rate: the increase in costs that affects your own lifestyle, spending habits and financial circumstances. Understanding that difference is important because inflation doesn't just affect what you spend today. It can also influence what your money is worth tomorrow.

Inflation's effect on wealth

Imagine leaving an ice cube outside on a warm afternoon. At first glance, it appears unchanged. Yet minute by minute, it gradually becomes smaller. Cash savings can behave in much the same way.

The balance shown on your bank statement may remain exactly the same, but if prices are rising faster than the interest you earn, the purchasing power of that money slowly begins to erode. This is particularly relevant for people holding larger cash balances, relying on a fixed income in retirement, or saving towards long-term goals. The challenge isn't necessarily that your money is disappearing. It's that over time, it may buy less than it once did.

Consider a pension that paid £1,000 a month in 2020. To provide the same spending power in April 2026, that income would need to have risen to around £1,304 per month (3). That's the reality of inflation.

Prices may rise gradually, but over several years their cumulative effect can become significant. It's one of the reasons that successful financial planning isn't simply about accumulating wealth. It's about preserving purchasing power and ensuring that wealth continues to support your lifestyle in the future.

Two practical ways to help protect your wealth

The good news is that protecting your wealth from inflation doesn't necessarily require dramatic changes. Often, small adjustments can make a meaningful difference.

-

Review your cash savings regularly

Many people haven't looked at their savings accounts for years. Unfortunately, banks don't always reward loyalty. Taking the time to compare rates and review where your cash is held could help ensure your money is working harder for you. This won’t eliminate the impact of inflation entirely, but it can help narrow the gap between rising prices and the growth of your savings. -

Consider whether all of your money needs to remain in cash

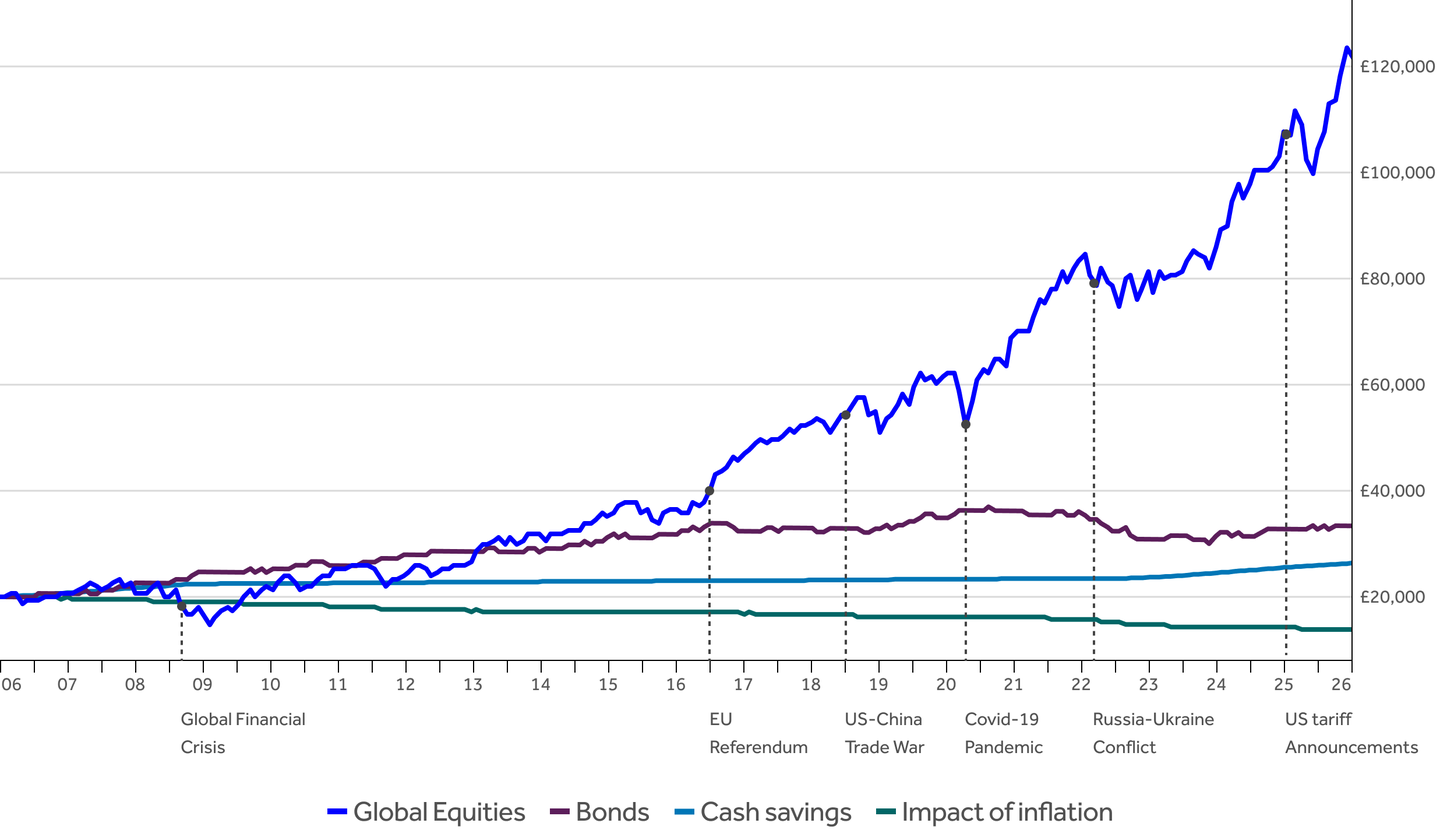

An emergency fund remains an important part of good financial planning. Knowing you have readily accessible savings should the unexpected happen can provide valuable peace of mind. Beyond that, however, it may be worth asking whether surplus cash is still serving a purpose. Investing involves risk and values can fall as well as rise. However, for money that is unlikely to be needed for many years, investing has historically offered greater potential for long-term growth than cash alone, as shown in the chart below.

Looking beyond the headlines

When inflation figures are announced each month, it's easy to focus on the number itself. Yet the more important question is often what that number means for your own circumstances. The truth is that no two households experience inflation in exactly the same way. Your spending habits, lifestyle, goals and long-term plans will ultimately determine how rising prices affect you.

This is why good financial planning isn't about reacting to every inflation announcement or economic headline. It's about building a strategy that can adapt to changing conditions while keeping your long-term objectives firmly in sight. After all, inflation may be measured using a standard basket of goods, but no two households ever fill their baskets in quite the same way.

Get in touch

At Titan Wealth, we can help you protect your wealth from inflation. If you’d like to speak to a wealth consultant to find out more, please contact us by emailing financialplanning@titanwci.com or calling 01534 724241.

Sources:

1. Office for National Statistics

2. Statistics Jersey

3. Bank of England