Summary:

-

The post-Global Financial Crisis investment environment of low inflation, falling interest rates and stable globalisation has materially changed.

-

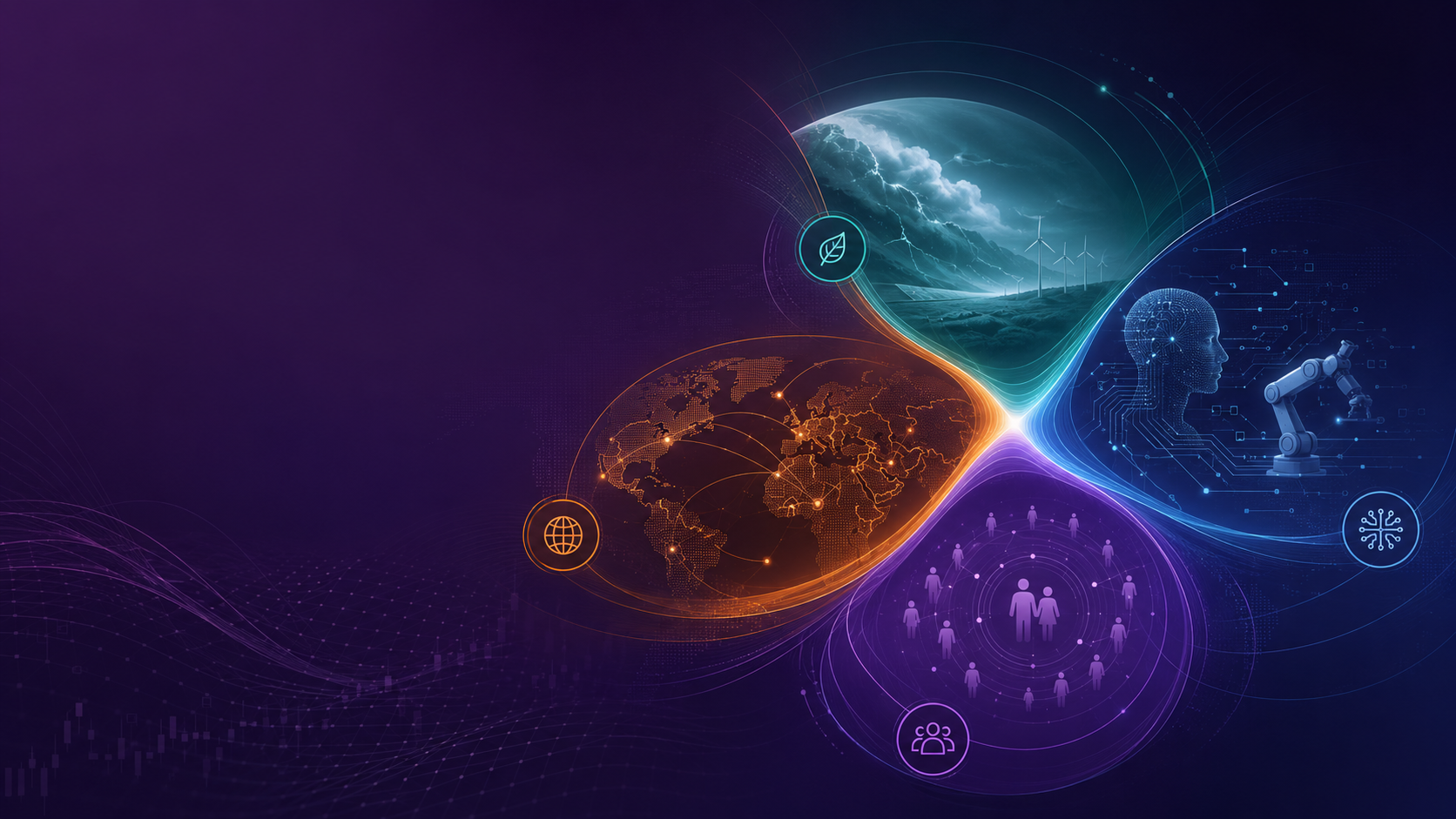

Four structural forces are reshaping markets and economies: geopolitical fragmentation, climate change, artificial intelligence and demographic shifts.

-

Investors may need to prepare for a world of higher inflation volatility, elevated interest rates, changing market leadership and greater geopolitical disruption.

-

Diversification across regions, asset classes, investment styles and structural themes is becoming increasingly important in a more fragmented and dynamic environment.

-

Long-term success is likely to favour investors who remain invested, adapt to the new regime and avoid relying solely on strategies that worked during the previous decade.

For much of the decade that followed the Global Financial Crisis, investors grew accustomed to a remarkably benign backdrop. Inflation was low, interest rates were close to zero, globalisation was expanding, labour was plentiful and central banks were usually on hand to cushion markets when conditions became more difficult.

It was not always an easy period, but it was a relatively predictable one. Investors could broadly rely on falling bond yields, strong US equity leadership, expanding global trade and policy support to smooth over many of the bumps in the road.

That world has not disappeared overnight, but it has changed materially. The investment environment we face today is more complex, more volatile and less forgiving. The challenge for investors is not simply to decide whether markets go up or down next month; it is to understand the structural forces reshaping the world economy and build portfolios that can cope with a wider range of outcomes.

Four forces sit at the heart of this new regime: geopolitics, climate change, artificial intelligence and demographics.

The first is geopolitical fragmentation. The relationship between the United States and China has moved from uneasy cooperation to strategic competition. This does not mean globalisation is dead. Trade is still happening, and in many areas it continues to grow. But the pattern of trade is changing. Countries and companies are increasingly prioritising resilience, security and political alignment over maximum efficiency.

That matters for investors. Supply chains, technology standards, energy security, artificial intelligence, defence spending and access to critical materials are all becoming more political. The old assumption of one integrated global economy is giving way to competing blocs and spheres of influence.

The second force is climate change. For many years, climate was discussed as a long-term environmental risk. It is now a present economic reality. Extreme weather events are affecting agriculture, insurance markets, infrastructure, transport networks and supply chains. At the same time, governments and companies are spending heavily on mitigation and adaptation, from renewable energy and grid infrastructure to flood defences and more resilient buildings.

This creates both risks and opportunities. Some assets will face higher costs, stranded asset risk or greater physical exposure. Others will benefit from sustained capital investment in energy transition, infrastructure renewal and resource efficiency.

The third force is artificial intelligence and robotics. Technological change is not new, but the current wave feels different. Previous industrial and digital revolutions enhanced human productivity. AI and robotics may go further by directly competing with both cognitive and physical labour.

That does not mean a jobless economy is imminent, but it does suggest that the balance of power between labour, capital and technology could shift again. Companies able to deploy AI effectively may enjoy lower costs, better productivity and stronger margins. Others may find their business models disrupted. As ever with new technology, the long-term winners may not be the same as the early market darlings.

The fourth force is demographics. For decades, the global economy benefited from an expanding labour force, helped by China’s integration into the world economy, the opening up of Eastern Europe and favourable population trends across many emerging markets. That tailwind is fading. Working-age populations are shrinking in many countries, dependency ratios are rising and governments face growing fiscal pressure from ageing societies.

In this context, automation and AI are not just exciting technologies; they may become necessary tools for economies trying to offset labour shortages and maintain productivity growth.

Together, these forces have important market consequences.

Inflation is unlikely to be as stable as it was in the pre-Covid decade. Even if the worst of the post-pandemic inflation shock is behind us, fragmented supply chains, higher defence spending, climate adaptation and labour scarcity do not obviously point to permanently low inflation. Interest rates may also remain higher than investors became used to during the 2010s.

Commodities may play a different role too. After a long period of relative stagnation, supply constraints, geopolitical disruption and renewed infrastructure investment could support a more favourable structural backdrop for selected real assets and resources.

Equity markets are also changing. The US remains central to global innovation, especially in AI, but the era of uninterrupted US exceptionalism should not be taken for granted. Market leadership has become more concentrated, passive investing has become increasingly dominant and the largest technology companies now exert a powerful influence over index returns.

This does not mean passive investing is broken. Low-cost index exposure remains a valuable tool. But investors should recognise that passive strategies are not neutral in every environment. They allocate more capital to what has already become large, and they can increase exposure to market concentration. In some areas, particularly less efficient equity markets and fixed income, skilled active managers may still have a meaningful role to play. Similarly, gaining exposure to structural themes alongside passive and more core active funds can be a powerful combination in the new environment.

So what should investors do in response to these changes?

The answer is not to retreat into cash. Cash can feel safe because its value appears stable from day to day. But over longer periods, inflation can quietly erode its purchasing power. The true risk is not always volatility; it is failing to preserve and grow real wealth.

Equities remain essential because they represent ownership of productive assets. Companies that can innovate, adapt, raise prices and compound earnings remain one of the best long-term defences against inflation and currency debasement. The path may be bumpier, but the case for owning businesses has not disappeared.

Diversification also matters more than it has for some time. Investors should think across regions, asset classes, styles and themes. Geography is becoming increasingly important, because political alignment, supply-chain positioning and energy security can all affect returns. Alternatives and real assets may also have a larger role to play where traditional bonds provide less reliable protection than they did in the past.

Finally, manager selection matters. Some investment processes were built for the old regime of low inflation, falling rates and abundant liquidity. Not all will adapt successfully. Investors should ask whether managers are simply repeating what worked in the last decade or have genuinely adjusted their frameworks for a more volatile and fragmented world.

The move from calm to chaos does not mean investors should be fearful. It means they should be realistic. The coming decade may be less predictable, but it will not be short of opportunity. The winners are likely to be those who remain invested, stay diversified, avoid over-reliance on yesterday’s assumptions and build portfolios capable of navigating a world that is more complex but also more dynamic.