AI has gone from a future concept to something most of us interact with almost daily, but building it at scale is another story altogether. The level of investment required is vast, with Goldman Sachs estimating that the AI buildout could require $6 trillion of cumulative capital expenditure by 2030, making this one of the biggest investment cycles since the 19th-century railway boom. Despite this, there is still a degree of uncertainty.

What is becoming clearer – and something we’ve highlighted previously – is where the early gains are showing up. The companies and economies supplying the hardware, components and infrastructure needed to make AI work are already seeing the impact, with emerging markets (“EM”) increasingly in focus.

Developed markets are increasingly constrained in their ability to support the AI buildout. Bottlenecks are emerging across chip manufacturing capacity, power availability, grid infrastructure and the physical data-centre space required to process rapidly expanding AI workloads. As these constraints intensify, more value is being pulled towards the EM companies that sit inside the AI supply chain.

This is already visible in market performance: year to date, the MSCI EM Index has returned around 25%, compared with roughly 8% for MSCI World. However, this is not a broad-based EM story. Returns have been heavily concentrated in two regions: Taiwan and South Korea.

AI demand is highly reliant on advanced chips, and Taiwan Semiconductor Manufacturing Company (“TSMC”) is the global leader in producing them. TSMC manufactures the chips designed by Nvidia, AMD, Apple and others, giving it exceptional pricing power and strategic importance within the AI supply chain. Taiwan sits at the centre of the global semiconductor industry, generating more than 60% of global foundry revenue and producing over 90% of the world’s leading-edge chips.

Advanced chips are only useful if they are supported by sufficient memory capacity. As large language models grow in size and adoption accelerates, demand for high-bandwidth memory is rising sharply. This places South Korean leaders such as SK Hynix and Samsung in a strong position. Both companies are central suppliers of the memory technology needed to support the next phase of the AI buildout and have been key drivers of South Korea’s recent market returns.

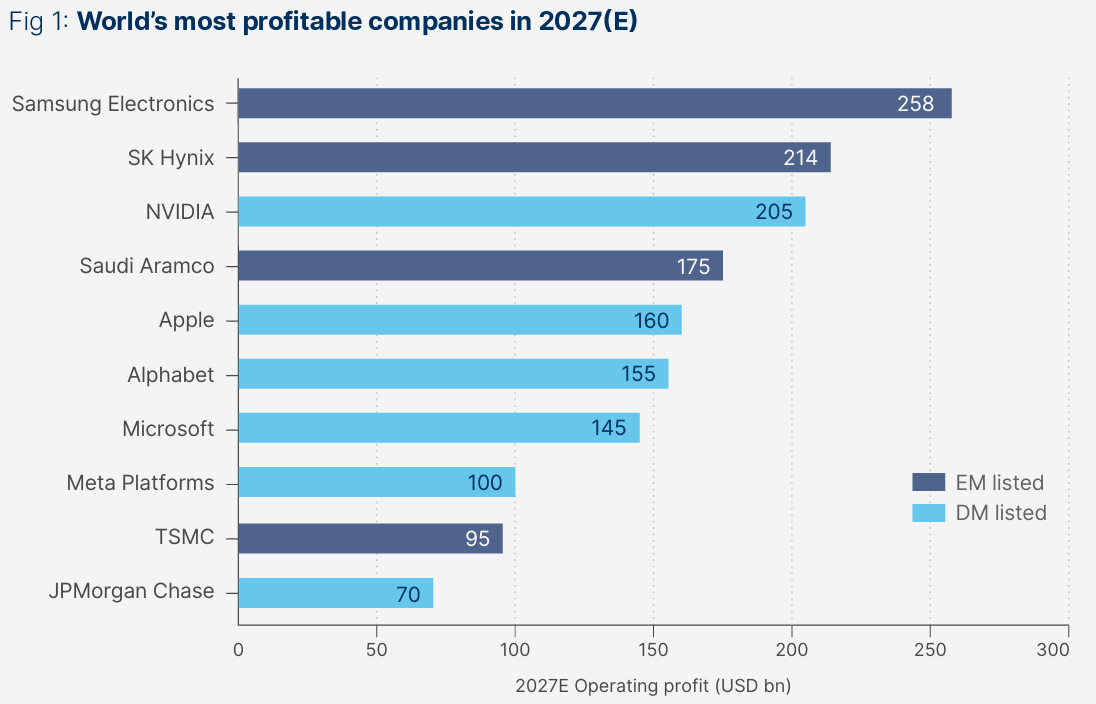

This concentration gives EM companies significant pricing power and strategic importance. As a result, a greater share of the value created by global AI spending may flow to Taiwan and South Korea, rather than remaining solely with US technology firms. The chart below highlights this shift, showing that TSMC, SK Hynix and Samsung are all expected to rank among the world’s 10 most profitable companies in 2027.

The hardware story is therefore only one side of the emerging market opportunity. Chips and memory explain why Taiwan and South Korea have led returns so far, but the next phase of the AI buildout also depends on where the physical infrastructure can be built, powered and scaled efficiently.

A further constraint sits in the data centres needed to power AI. North America currently accounts for approximately 45-50% of global data centre capacity, while EMs account for less than 10%. However, total capacity is expected to nearly double by 2030, from around 103GW to roughly 200GW, requiring a major increase in available power. The US is already facing delays linked to power availability, creating an opportunity for regions such as India, Southeast Asia, Latin America and the Middle East to attract a growing share of new data-centre investment.

Ultimately, AI may be a developed-market-led theme in terms of end demand, but the infrastructure required to support it is increasingly global. The companies enabling this buildout, from advanced chip manufacturers in Taiwan, to memory leaders in South Korea, and potentially data-centre hubs across India, Southeast Asia, Latin America and the Middle East, are becoming more strategically important to the AI value chain.

This does not mean emerging markets will benefit evenly, but it does suggest the next phase of AI returns may be less about who owns the best applications, and more about who supplies the physical foundations that allow them to scale. Through our EM allocation in the Titan Global Growth Fund, which includes exposure via Aubrey Emerging Market Opportunities and therefore high-quality growth companies across EM, we are already positioned to access high-quality growth companies linked to Asian technology supply chains and the broader AI buildout.