When I sat down to write this article, I made a conscious decision to steer clear of three topics that have dominated news flow in recent months - the conflict in the Middle East, AI, and the Trump administration. They are all enormously important, but they share one characteristic that makes them difficult to write about with any confidence right now. Matters are moving so rapidly on all three fronts that any considered analysis would likely be outdated before the proverbial ink is dry. What I wanted instead was a theme that tends to go under the radar, that is underappreciated, but that will matter enormously over the coming years. That theme is copper.

It may not carry the safe haven appeal of gold or silver, the scarcity story of platinum or the coverage that lithium attracts in relation to electric vehicles. It is the wire in the walls, the pipe under the street, the component nobody thinks about until it stops working. As investment themes go, it is about as understated as it gets. But the world needs copper in quantities that were difficult to imagine a decade ago, and the mining industry is struggling to keep up. That gap between demand and supply is widening, and the drivers behind it are not short-term cyclical forces. They are the defining infrastructure themes of the next 20 years.

I hope you’ll forgive me that two of its most powerful demand drivers are the very topics I was trying to avoid writing about.

Let’s start with AI. The data centres running the next generation of AI chips are quite literally the most power-hungry buildings ever constructed. A single AI server rack now draws ten times the electricity of a conventional server, and the environments that they run in make copper non-negotiable. Importantly, US data centre electricity consumption is projected to grow from around 5% of total grid demand today to 14% by 2030. That is almost triple the demand and (somewhat scarily) is only four years away.

Alongside AI, we are undoubtedly living through a decade of sharply rising geopolitical tension, and that is reshaping defence budgets in ways that matter directly for copper. Modern warfare is no longer primarily mechanical. It is electrified. For example, a single Trident nuclear submarine contains around 90 metric tonnes of copper. Defence demand for copper is projected to triple by 2040, and crucially, that procurement is entirely price-insensitive. Governments do not delay submarine programmes because prices in materials like copper have moved. The US government's decision in late 2025 to formally designate copper as a critical mineral reflects precisely this shift in strategic thinking, and European rearmament is adding further weight to an already substantial demand picture.

The energy transition adds to things further still. Electric vehicles use roughly four times the copper of a conventional petrol car, and a single electric bus requires close to 370kg of the metal. Renewable energy infrastructure needs significantly more copper per unit of capacity than a gas-fired power station. Generating a megawatt from an offshore wind farm, with its turbines spread across miles of ocean and connected by heavy submarine cabling back to the mainland grid, requires up to 12 times more copper than generating it from a single gas plant. For context, a megawatt is roughly enough electricity to power around 800 homes. Scale that across the thousands of wind and solar projects planned globally over the next two decades and the numbers become meaningful very quickly.

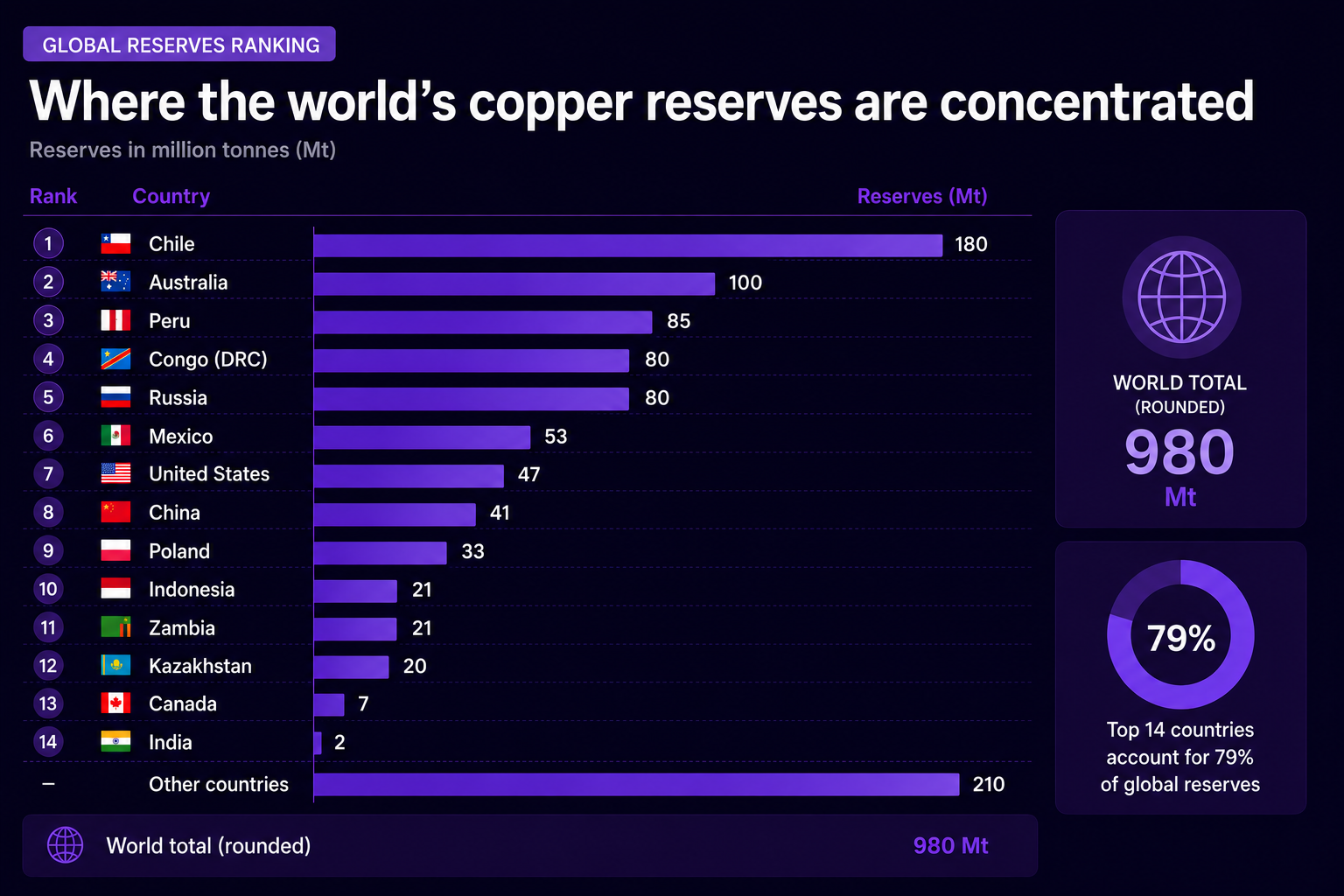

Supply is the problem. It takes an average of 17 years from discovery of a copper deposit to first production. A mine greenlit today will not start producing until the early 2040s. Ore grades at existing mines have fallen to around 0.4%, meaning vastly more rock must be processed to produce the same output. Chile, the world's largest producer, is experiencing a multi-decade drought that is curtailing operations and forcing miners to spend billions on desalination infrastructure just to maintain existing levels. China controls roughly 40% of global smelting capacity, meaning the physical route from mine to market runs through a rival geopolitical power. Treatment and refining charges turned negative in late 2025, a signal of just how tight the raw material pipeline has become.

As Rio Tinto’s Chair Dominic Barton stated in their latest results earlier this month “Nations are focusing ever more intensely on minerals and metals… the materials we provide not only fuel modern life but also enable underlying infrastructure for the technology revolution and energy transition”.

Copper will never generate the headlines that gold or bitcoin attract. But the structural case for the metal that physically connects the modern economy is building quietly. Sometimes the most interesting opportunities are the ones that nobody is talking about. Should you wish to discuss options for investing in to copper or mining, please speak to a member of the Advisory Stockbroking team who will be happy to assist.