"I do not like debt and do not like to invest in companies that have too much debt, particularly long-term debt. Increases in interest rates can drastically affect company profits and make future cash flows less predictable." — Warren Buffett

For much of the last decade, investors viewed the largest technology companies as the epitome of financial strength: cash-rich businesses generating enormous free cash flow with little reliance on external financing. The AI revolution may be changing that perception. As competition to build next-generation infrastructure intensifies, these companies are taking on increasing amounts of debt, raising an important question for bond investors: are hyperscalers beginning to push the limits of their credit quality in pursuit of AI dominance?

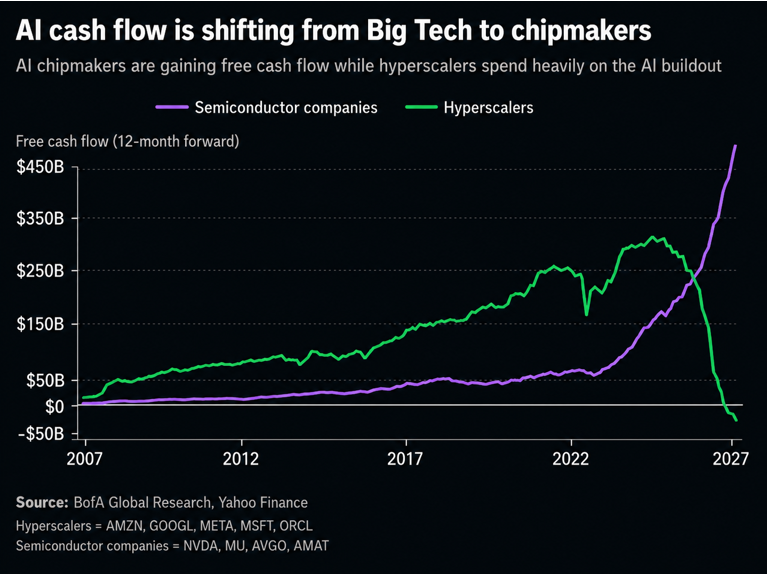

The below visual in a recent Bank of America Research piece, which illustrates the 12-month forward free cash flow (“FCF”) of the predominant players in the build-out of AI infrastructure, provides a thought-provoking representation of the scale and speed at which an enormous transfer of capital is taking place.

While it is not my intention to debate whether we are headed towards a 1999 dotcom-style market crash, it is worth considering the implications that this deployment of capital is already having on bond markets.

The large hyperscale technology companies have been raising billions of dollars to fund the build-out of their AI infrastructure. Historically, these companies essentially funded their growth through profits and FCF, with capital expenditure (“capex”) requirements being relatively limited due to the nature of the sector. However, the surge in computing power requirements has driven a corresponding increase in investment, most notably in the construction of large-scale data centres. Now, a proportion of the funding of these projects is currently being funded through operating cash flows and by raising additional equity, though, the hyperscale’s have increasingly been issuing debt to meet the funding needs.

As an indication of the scale involved, Morgan Stanley has forecast that AI-related debt issuance by hyperscale’s will top $500 billion globally, which is arguably a conservative estimate, with other estimates being upward of $750bn. As a reflection, Amazon recently raised $25bn, taking its total over the last 12 months to $107bn, while Alphabet has raised $85bn in debt and Oracle $43bn.

Unsurprisingly, the rapid accumulation of debt alongside sharply declining projected FCF has the potential to create challenges. Rating agencies, who have been criticised in the past for being slow to react, have recognised these risks. S&P Global Ratings downgraded Oracle’s long-term issuer credit rating last week to BBB-, one notch above Junk.

S&P Global Ratings said the downgrade was driven mainly by Oracle’s rapidly rising capital expenditure, which is forecast to reach $95bn in 2027, and its widening cash deficit, with free operating cash flow expected to deteriorate to negative $42bn that year.

The amount of debt being raised is also having a profound effect on bond markets generally and the make-up of bond indices. Banks have traditionally been the predominant sector in investment grade bond indices, however, AI-related supply is transforming the technology sector into one of the largest constituents alongside financials. The risk is financial firms and smaller corporate borrowers may face the risk of being “crowded out” as a finite amount of investor capital is competed for, forcing these borrowers to have to increase yields to attract investor capital.

While hyperscaler bond issuance has so far been easily absorbed in 2026, it has reached record levels among AA-rated issuers. With US investment grade spreads still trading at particularly tight levels, investors may eventually demand higher spreads to absorb the growing supply of debt. Companies are seemingly cognisant of this dynamic and have increasingly issued debt in non-USD denominated tranches. Against this market backdrop and given the growing risks in bond markets associated with substantial AI-related spending, we believe an active approach to fixed income allocation is sensible. This helps avoid being forced to own bonds from highly indebted issuers simply because they carry a large weighting in a passive index. It also gives managers that we invest with the ability to be flexible in their stock selection from a sector, credit, currency and issuer type perspective. At this stage of the market cycle, we also believe it is paramount to remain cautious and selective when taking on duration risk.